According to the Indian Cyber Crime Coordination Centre (I4C), cyber frauds may cause losses exceeding ₹1.2 lakh crore in 2025. India is actively adopting AI-driven tools like MuleHunter.AI and the Pratibimb app to detect illicit mule accounts.

The Indian Cyber Crime Coordination Centre (I4C) signed an MoU with the RBI to create a real-time system to identify and block illegal "mule accounts" used by cybercriminals.

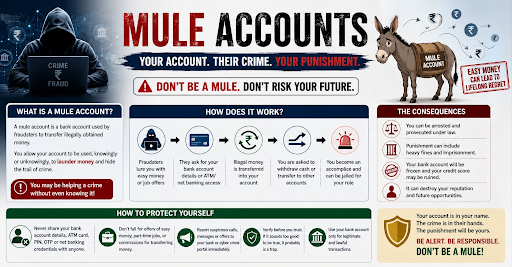

Mule accounts are bank accounts used by cybercriminals to receive, transfer, and launder illegally obtained money.

It acts as structural intermediaries, breaking the data trail between fraudsters and their victims to obscure the origins of stolen funds.

Categories: Participants divide into three specific groups:

Layering Funds: Fraudsters route money from cybercrimes (like phishing, online scams, or investment fraud) directly into a mule account

Rapid Splitting: The funds are quickly moved out—either routed through a chain of other mule accounts, converted into cryptocurrency, or withdrawn as physical cash.

Evading Detection: Because the account belongs to a legitimate citizen, it hides the true identity of the criminal network from law enforcement tracking.

Digital payment explosion: Rapid financial inclusion through the JAM trinity (Jan Dhan, Aadhaar, Mobile) and cheap data, achieving 22.35 billion UPI transactions in April 2026 alone.

Flexible onboarding loopholes: Fraudsters exploit the availability of multiple identity permutations, as current rules allow an individual to procure up to nine SIM cards using a single Aadhaar card.

Targeting vulnerable demographics: Transnational syndicates target unemployed youth, students, and first-time digital banking users using automated, bot-driven fake job offers on platforms like Telegram and WhatsApp.

Siloed institutional operations: Banks separate their Anti-Money Laundering (AML) and Fraud teams, leading to fragmented intelligence and an inability to halt mule transactions in real-time.

Financial losses: In 2024, India recorded 36 lakh cyber fraud cases, resulting in losses exceeding Rs. 22,845 crore.

Macro-economic threat: Annual financial losses due to cyber-enabled frauds exceed Rs. 1.2 lakh crore in 2025, which amounts to 0.7% of India's GDP.

Erosion of public trust: Increase in financial fraud induces severe mental distress for victims and undermines trust in the digital banking ecosystem.

Collateral damage to innocent citizens: Poor transaction monitoring causes banks to wrongfully freeze the accounts of innocent individuals and small businesses.

AI-driven detection integration

The Indian Cyber Crime Coordination Centre (I4C) and the Reserve Bank Innovation Hub (RBIH) signed an MoU to deploy MuleHunter.ai, a machine-learning system that identifies suspicious account behavior across the banking sector.

Real-time GIS tracking

Police forces deployed the Pratibimb App to map cybercriminals using real-time Geographic Information System (GIS) tracking linked to fraudulent mobile numbers.

Telecom infrastructure crackdowns: The Department of Telecommunications (DoT) mandated Aadhaar for new SIM cards and blocked over 4.2 crore SIM cards to disrupt mule communication networks.

Criminalize mule activity

Amend the Prevention of Money Laundering Act (PMLA) to define and penalize money mule operations as standalone crimes, aligning with global standards in the UK and Australia.

Unify banking frameworks

Financial institutions must merge their siloed AML and Fraud functions so they treat mule networks as money laundering infrastructure rather than isolated fraud anomalies.

Deploy graph analytics:

Implement network-level monitoring utilizing graph analytics to detect structured fund dispersal across multiple connected accounts instead of relying solely on individual transaction thresholds.

Improve cross-institutional intelligence

Regulators must establish proactive, SWIFT-style cross-institutional intelligence sharing mechanisms to help banks trace and intercept illicit funds before transfers complete.

Combating mule accounts requires shifting from isolated rules to a network-centric strategy that integrates advanced AI, strict legal penalties, and real-time cross-institutional data sharing.

Source: NEWSONAIR

|

PRACTICE QUESTION Q. The 'Pratibimb App', recently seen in the news, is best described as: (a) A real-time gross settlement system managed by the RBI. (b) A GIS-based software tool designed to track cyber criminals. (c) A platform for monitoring Non-Performing Assets (NPAs) in scheduled commercial banks. (d) A biometric authentication app for accessing public distribution services. Answer: (b) Explanation: The 'Pratibimb' app is a Geographic Information System (GIS) software developed by the Jharkhand Police CID in collaboration with the Union Home Ministry's Indian Cyber Crime Coordination Centre (I4C). It maps the real-time locations of mobile numbers linked to cybercrimes, allowing law enforcement agencies to quickly identify and apprehend digital fraudsters. |

According to the Reserve Bank of India (RBI), a mule account is a bank account used by criminals to launder illicit funds, often set up by unsuspecting individuals lured by promises of easy money or coerced into participation.

The financial impact is massive and growing. According to the Indian Cyber Crime Coordination Centre (I4C), the annual loss due to cyber-enabled frauds may exceed ₹1.2 lakh crore in 2025, which amounts to 0.7% of India’s GDP. Furthermore, in FY24 alone, Indian citizens reported losses of over ₹22,845 crore to cyber financial frauds (Source: I4C).

MuleHunter.AI is an AI-driven fraud detection model developed by the Reserve Bank Innovation Hub (RBIH) to analyze patterns of account activity and eliminate mule accounts. Under a recent MoU, the I4C will share intelligence from its Suspect Registry to train and enhance this AI model across banks (Source: Ministry of Home Affairs).

© 2026 iasgyan. All right reserved