India's FY26 outward remittances under the Liberalised Remittance Scheme decreased by two percent to $29 billion. Strict visa regimes and rupee depreciation reduced travel and education spending, while asset-backed investments in global equities, debt, and foreign property surged significantly

India's outward remittances under the RBI's Liberalised Remittance Scheme (LRS) dropped by 2% to $29 billion in FY26.

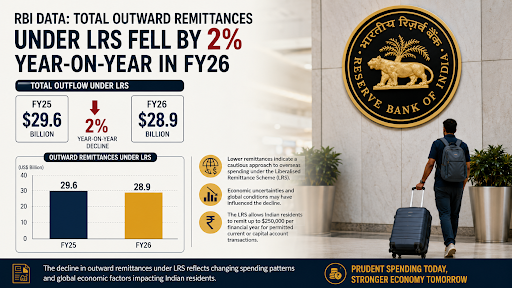

It is a framework, established by the Reserve Bank of India (RBI), that allows resident individuals, including minors, to legally remit up to $250,000 per financial year for permitted current or capital account transactions.

The RBI introduced the scheme in 2004 with an initial limit of $25,000, which has been revised in stages to reflect prevailing macro and microeconomic conditions.

Permitted Transactions: Individuals utilize the scheme for purposes such as education, travel, medical treatment, gifts, maintenance of close relatives, and overseas investments in equity, debt, or immovable property (Source: RBI).

Monitoring Mechanism: Authorized dealer banks track every remittance against the individual's Permanent Account Number (PAN) and report these transactions directly to the RBI.

Overall Contraction: Total outward remittances under LRS witnessed a 2% decline, dropping to $28.98 billion in FY26 from $29.56 billion in FY25. (Source: RBI)

Education Spend Declined: Funds remitted for overseas education fell by about 20.9% year-on-year to $2.31 billion in FY26. (Source: RBI)

Visa and Employment Hurdles: Stricter visa regimes in the United States and other major markets, coupled with weaker job opportunities abroad, deter students from pursuing foreign degrees.

Travel Moderation: International travel remittances slipped 2.3% to $16.87 billion in FY26 as rupee depreciation and geopolitical uncertainty forced citizens to reconsider high-cost travel plans.

Strict Annual Limits

The RBI enforces a strict cap (Currently $250,000) for maintenance and gifts; however, it permits remittances exceeding this amount for education and medical treatment when supported by specific documentation.

Purpose Code Classification

The RBI mandates specific codes for transactions: S1301 for family maintenance, S1302 for gifts, and S1107 for education tuition to ensure FEMA compliance.

Tax Collected at Source (TCS) Reforms: The Union Budget 2026-27 reduced the TCS rate on LRS for education and medical expenses from 5% to 2%.

High-Value Remittances: Remittances for purposes other than education and medical treatment that exceed ₹10 lakh in a financial year attract a 20% TCS rate.

Maintenance Eligibility: Only "close relatives"—defined by the Companies Act 2013 as parents, spouse, children, and siblings—qualify for maintenance remittances under code S1301.

India’s remittance ecosystem in FY26 reflects a shift from discretionary consumption to strategic global investment amid heightened external volatility and a national push for economic austerity.

Source: THEHINDUBUSINESSLINE

|

PRACTICE QUESTION Q. Consider the following statements about the Liberalised Remittance Scheme (LRS):

Which of the statements given above is/are correct? a) 1 and 2 only b) 1 and 3 only c) 2 and 3 only d) 1, 2, and 3 Answer: b Explanation: Statement 1 is CORRECT: Under the Reserve Bank of India's (RBI) Liberalised Remittance Scheme (LRS), resident individuals (including minors) can legally remit up to USD $250,000 per financial year for permissible current and capital account transactions. Statement 2 is INCORRECT: The "family maintenance" purpose code applies strictly to close relatives (as defined under the Companies Act). Remittances to cousins or friends for their day-to-day living do not qualify for this code and must be classified as a "Gift" (S1302) instead. Statement 3 is CORRECT: Under Income Tax rules on LRS, the TCS threshold stands at ₹10 lakh. Any amount exceeding this ₹10 lakh limit in a financial year for purposes other than education and medical treatment attracts a 20% Tax Collected at Source (TCS). |

The LRS is an RBI framework that allows resident Indians to legally remit up to USD 250,000 per financial year (April–March) abroad for permitted purposes such as travel, education, medical treatment, family maintenance, gifts, or investments.

Total LRS outflows contracted by about 2% to $29 billion in FY26 primarily due to a 20.9% plummet in overseas education spending and a 3.1% dip in international travel, heavily influenced by rupee depreciation and strict visa restrictions.

Education costs have surged drastically; for example, an undergraduate degree at Harvard that cost ₹53 lakh in 2021 now costs nearly ₹78 lakh, marking a 47% increase due to rupee depreciation and 10-12% annual overseas education inflation.

© 2026 iasgyan. All right reserved