To stabilize the rupee and bridge the balance of payments deficit, India has eliminated capital gains and withholding taxes on FII investments in government bonds via the Income Tax Amendment Ordinance 2026, boosting foreign debt inflows and lowering imported inflation.

Why In News?

Government promulgated the Income Tax Amendment Ordinance, 2026, scrapping capital gains and withholding taxes on Foreign Institutional Investors' (FIIs) investments in government bonds to attract foreign capital.

Who are Foreign Institutional Investors (FIIs)?

FIIs are large international organizations—such as hedge funds, mutual funds, pension funds, insurance companies, and investment banks—that invest pooled capital into financial markets outside of their home country.

The Central Government officially specifies Foreign Institutional Investors (FIIs) by notification under Section 210(6)(a) of the Income-tax Act, 2025.

The Securities and Exchange Board of India (SEBI) registers Foreign Portfolio Investors (FPIs), who actively operate as notified FIIs in the Indian financial markets.

Recent Trends: FII investments in Indian government securities currently stand at ₹3.75 lakh crore, representing 3.34% of the total outstanding stock of ₹112.42 lakh crore.

Foreign investors aggressively sell Indian equities, pulling out 28 billion in 2026 and 47 billion since 2024, while simultaneously injecting $26 billion into the Indian debt market.

What Recent Changes Government Announced?

The Government issues the Income Tax Amendment Ordinance, 2026, coming into full effect from April 1, 2026, to make the sovereign debt market highly attractive to overseas capital.

The ordinance completely exempts FIIs and the Bank for International Settlements (BIS) from paying capital gains tax (both short-term and long-term) and withholding tax on interest income earned from government securities.

The Reserve Bank of India (RBI) simultaneously expands the Fully Accessible Route (FAR) to include all new issuances of 15-year, 30-year, and 40-year government securities.

The RBI also removes all previous limits pertaining to short-term investment and concentration for FPIs investing under the General Route.

|

What is Withholding Tax? Withholding Tax (WHT) operates as an advance tax collection mechanism where the payer deducts the tax directly at the source before transferring the income, such as interest or dividends, to the recipient. |

Why is India Offering Tax Relief to Foreign Institutional Investors?

India faces severe capital flight and a looming Balance of Payments (BoP) deficit estimated between $40 billion to $60 billion for FY26 and FY27.

Rising crude oil prices, triggered by the Iran war, strain India's foreign exchange reserves and cause steep depreciation of the Indian Rupee.

High tax friction, including a 30% short-term capital gains tax and 12.5% long-term capital gains tax, actively deters foreign investors and hinders India's meaningful inclusion in global bond indices.

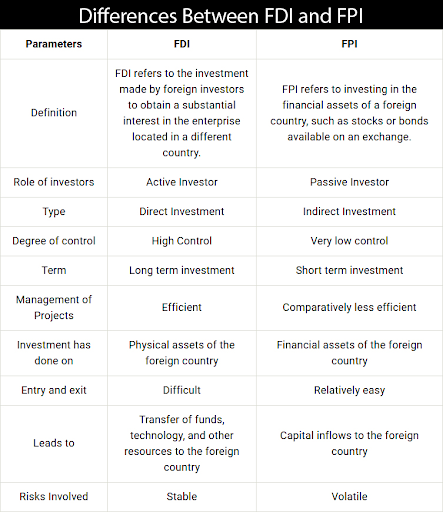

Weak Foreign Direct Investment (FDI) and FPI equity outflows force policymakers to rely on strong debt inflows as a crucial external sector stabiliser.

Expected Impact on Indian Economy

The tax exemption increases net returns for FPIs investing in Indian government securities by 15-20%, boosting India's global debt market competitiveness.

Economists project foreign inflows of $45-50 billion into government debt over the next two years, effectively bridging the targeted BoP gap.

The Indian Rupee strengthens immediately, jumping 50 paise to ₹95.30 per US dollar, which directly combats imported inflation by lowering the domestic costs of crude oil and electronics.

The influx of foreign capital increases bond demand, pushing the benchmark 10-year government bond yield down to 6.96% and lowering the cost of borrowing for both the government and public sector undertakings.

Source: INDIANEXPRESS

|

PRACTICE QUESTION Q. Consider the following statements regarding the taxation of Foreign Institutional Investors (FIIs) in India:

Which of the statements given above is/are correct? (a) 1 only (b) 2 only (c) Both 1 and 2 (d) Neither 1 nor 2 Answer: (c) Explanation: Statement 1 is correct: The ordinance exempts Foreign Institutional Investors (FIIs) from tax on both interest income and capital gains arising from investments in Indian government securities. Statement 2 is correct: The same income-tax exemption has also been explicitly extended to the Bank for International Settlements (BIS) for investments in these debt instruments. |

Foreign Institutional Investors are large overseas financial organizations—such as mutual funds, hedge funds, insurance companies, and pension funds—that actively invest capital into the financial markets of a country outside their home base.

Withholding tax is a regulatory income tax deducted at the source by the payer before distributing interest or dividend earnings to the investor.

Government Securities are sovereign debt instruments issued by the central or state governments to borrow funds directly from the public and institutional investors while guaranteeing fixed interest payments.

© 2026 iasgyan. All right reserved