The era of cheap global money is ending, triggering foreign capital outflows and Rupee depreciation. However, India's robust macroeconomic fundamentals, domestic market reliance, and recent inclusion in the JPMorgan global bond index provide vital resilience against global liquidity shocks.

The Reserve Bank of India officially flags concerns over elevated global sovereign bond yields and the end of the cheap global money era.

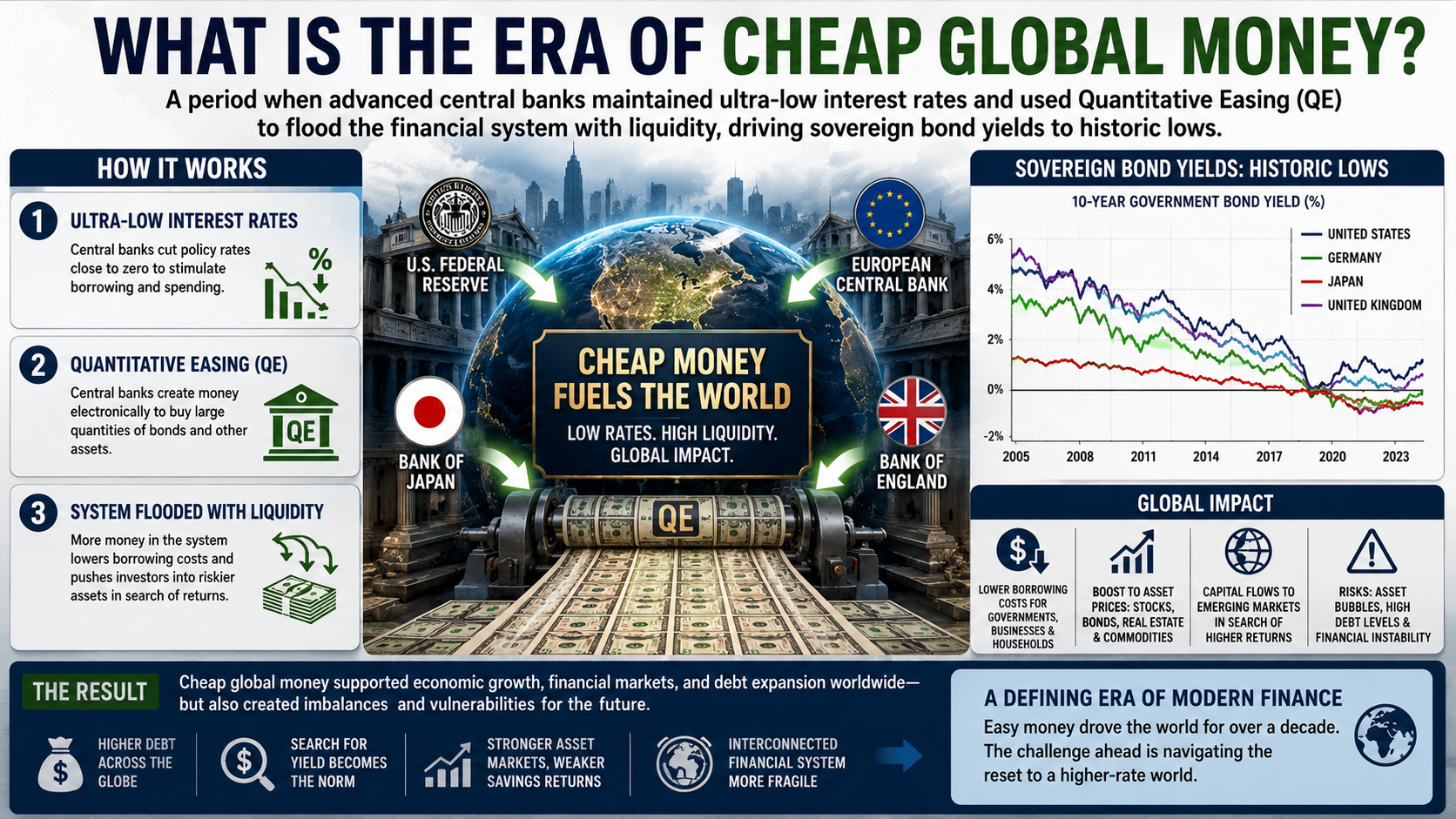

Cheap global money defines an economic era where central banks execute Quantitative Easing (QE) and maintain ultra-low interest rates to stimulate economic growth.

Central banks purchase government bonds and mortgage-backed securities, flooding the financial system with abundant global liquidity.

This monetary accommodation drives sovereign bond yields to historic lows, pushing the US 10-year yield to 0.9%, the UK yield to 0.4%, and the Japanese yield to negative territory during the 2020-21 pandemic.

The strategy purposefully makes government debt cheaper, encouraging global banks to lend more capital to consumers and businesses.

India attract foreign capital inflows as global investors search for higher-yielding emerging market assets.

The Indian economy records unprecedented capital surges, securing an average of $67.3 billion annually in net capital flows between 2009-10 and 2023-24.

Foreign Portfolio Investors (FPIs) pour billions into Indian equities and debt markets, profiting from the highly favorable interest-rate differential.

This abundant dollar liquidity strengthen India's Forex reserves, strengthens macroeconomic stability, and fuels domestic economic expansion.

Multiple severe global shocks revive acute inflationary pressures, heavily driven by COVID-19 supply chain disruptions, the Russian invasion of Ukraine, US trade tariffs, and the West Asia conflict.

Central banks abruptly terminate Quantitative Easing, declaring previous ultra-low interest rates entirely unsustainable against sticky inflation.

Governments issue excessive public debt, forcing financial markets to demand higher returns for risk.

The US Federal Reserve maintains a "higher-for-longer" policy, pushing the US 10-year Treasury yield up to roughly 4.5% to 4.6%.

The yield differential between India's 10-year bond and the US Treasury narrows to approximately 250 basis points, plunging below the historical decade average of over 400 basis points.

Foreign investors withdrew ₹27000 crore from Indian equities in May, totaling ₹2.2 lakh crore in 2026.

Diminished foreign capital inflows limit foreign exchange availability, exerting direct downward pressure on the Indian Rupee (INR).

Indian corporations face higher external borrowing costs when raising funds from international credit markets.

Unhedged foreign investors lose their essential yield cushion, as the narrow interest rate advantage fails to compensate for ongoing currency depreciation risks.

Currency Depreciation: Persistent capital flight drives the Rupee down by 10.96% in FY26, breaching the US$95 mark against the dollar.

Imported Inflation: A weaker Rupee makes essential imports more expensive. As per RBI estimates, a 5% depreciation in rupee can increase headline inflation by 35 basis points.

Widening Current Account Deficit (CAD): The toxic combination of capital outflows and elevated global crude oil prices threatens to push India's CAD to 2% of GDP in FY27.

Depletion of Forex Reserves: The Reserve Bank of India (RBI) sells dollars in the spot market— over US$53 billion between March 2025 and January 2026—to defend the Rupee from freefall.

Financial Market Volatility: Heavy FPI withdrawals trigger sharp fluctuations in equity markets and push domestic bond yields higher, steepening the yield curve.

Executes targeted market interventions to control currency volatility while building Forex reserves as a macroeconomic buffer.

Develop and deepen domestic bond markets, capitalizing on India's inclusion in the JPMorgan Emerging Market Global Diversified Index, which guarantees $20 billion to $25 billion in passive global capital inflows.

Implements comprehensive structural reforms across labor, land, and capital markets to enhance India's global manufacturing competitiveness.

Public and private corporations must diversify their funding sources to shield operations from sudden spikes in international borrowing costs.

Finalizes strategic trade agreements, such as the India-US trade deal, to eliminate tariff barriers and structurally support the Rupee against depreciation.

India systematically neutralizes the risks of a shrinking global liquidity era by fortifying domestic bond markets, accelerating structural reforms, and leveraging passive index inclusions to ensure resilient, self-reliant economic growth.

Source: INDIANEXPRESS

|

PRACTICE QUESTION Q. Discuss the macroeconomic implications of the "end of the cheap global money era" on emerging economies like India. 150 words |

The era of cheap global money represents a period when advanced central banks maintained ultra-low interest rates and utilized Quantitative Easing (QE) to flood the financial system with liquidity, driving sovereign bond yields to historic lows.

The era is ending because severe global supply chain disruptions, geopolitical conflicts, and rising commodity prices revive sticky inflation. Consequently, central banks abruptly terminate Quantitative Easing and hike interest rates.

The Reserve Bank of India actively intervenes by selling dollars from its Forex reserves in the spot market. It caps the Net Open Position in INR (NOP-INR) for banks at $100 million to curb speculative currency fluctuations.

© 2026 iasgyan. All right reserved