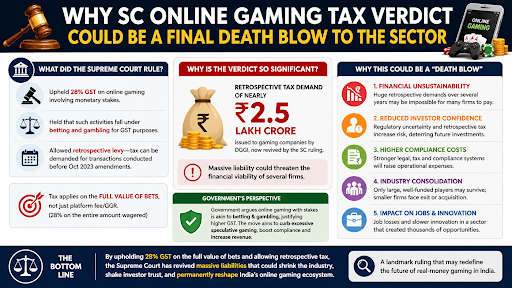

The Supreme Court upheld a 28% retrospective GST on the full face value of online gaming bets and affirmed states' rights to ban such games. This shift to a turnover taxation model threatens the Real Money Gaming (RMG) industry's financial survival.

Why In News?

The Supreme Court upheld the constitutional validity of levying a 28% retrospective Goods and Services Tax (GST) on the full face value of bets placed on online gaming platforms.

|

Read all about: ONLINE GAMING REGULATION IN INDIA l ONLINE GAMING AUTHORITY OF INDIA (OGAI): ORIGIN, FUNCTION, POWER l REGULATION OF ONLINE REAL MONEY GAMING IN INDIA l |

What Is the Background of the Online Gaming Tax Dispute?

Historical Tax Differentiation

Initially, the tax regime levies an 18% Goods and Services Tax (GST) on the Gross Gaming Revenue (GGR) or platform fees for games of skill, while taxing games of chance (gambling) at 28% on the total turnover.

GST Council Amendments (2023)

The government amends the CGST (Central Goods and Services Tax) Act to impose a flat 28% tax on the full face value of bets for all online gaming, ignoring the skill-versus-chance distinction.

Retrospective Tax Demands

Tax authorities issue retrospective show-cause notices totaling over ₹1 lakh crore against major gaming platforms, claiming that games involve "actionable claims" equivalent to betting.

Industry Challenge

Gaming companies challenge this move, arguing that courts historically protect games of skill under Article 19(1)(g) of the Constitution, and taxing the entire bet pool makes business commercially unviable.

What Is the Supreme Court’s Verdict on Online Gaming?

Upholds Retrospective Tax

The Supreme Court validates the government's decision to levy a retrospective 28% GST on the full face value of bets placed on real-money gaming platforms.

Defines Actionable Claim

The Court rules that online gaming platforms are not mere intermediaries; their activities generate taxable actionable claims.

Blurs Skill and Chance

The bench holds that wagering money on uncertain outcomes constitutes betting and gambling under the GST framework, regardless of whether the game involves skill or chance.

Clarificatory Amendments

The Court treats the 2023 GST amendments as merely clarificatory in nature, thereby justifying the retrospective application of the tax demands.

Upholds State Bans

In a separate ruling, the Court affirms the rights of state governments to enact laws prohibiting online money gaming within their specific jurisdictions.

What are the Impacts of the Supreme Court Verdict on Stakeholders?

Financial Crisis

Companies face massive tax liabilities (often exceeding their total historical revenues or bank balances), forcing many into voluntary liquidation or bankruptcy.

Job Losses

The sudden tax burden triggers severe workforce reductions, including massive layoffs, hiring freezes, and complete operational shutdowns across the sector.

Business Model Shift

Surviving industry giants shifting their business models away from real-money gaming toward non-gaming sectors like stockbroking or short-video apps.

Investor Panic

The verdict erodes investor confidence, causing immediate stock market crashes (e.g., Delta Corp shares fell 16%) and halting critical foreign direct investment (FDI) into the sector.

What Are the Arguments Supporting Higher Taxation?

Deters Social Evils

A high tax rate discourages addictive behaviors, protecting the youth and preventing the financial ruin of families associated with gaming addictions.

Boosts Public Exchequer

The 28% levy promises massive revenue generation for the government, with estimates projecting up to ₹20,000 crore annually.

National Security and Compliance

The strict tax and regulatory framework curbs money laundering, illegal offshore fund transfers, and the illicit use of cryptocurrencies on gaming platforms.

Taxation of Uncertain Outcomes

The government maintains that pooling money on uncertain events intrinsically constitutes betting, meaning the full deposit represents the true taxable value.

What Are the Arguments Against the Tax Regime?

Destroys Commercial Viability

Taxing the entire turnover (stake value) instead of the platform fee (GGR) creates a tax burden that far exceeds actual operator revenues, effectively acting as a de-facto ban.

Violates Fundamental Rights

The regime infringes upon Article 19(1)(g) by treating protected skill-based trades identically to gambling, rendering it a colourable legislation that indirectly destroys legitimate business.

Arbitrary

Applying a retrospective tax equates to "confiscatory taxation," violating Article 14 due to its excessive, disproportionate, and capricious impact on companies.

Promotes Illegal Grey Markets

Onerous tax rates drive operators and consumers away from regulated platforms and into unlicensed, illegal, or offshore grey markets, ultimately resulting in state revenue loss.

Conclusion

The Supreme Court's validation of the 28% retrospective GST legally settles the tax dispute but triggers an existential crisis for the online gaming industry, demanding urgent policy intervention to balance revenue generation with economic survival.

Source: INDIANEXPRESS

|

PRACTICE QUESTION Q. The transition from a Gross Gaming Revenue (GGR) model to a turnover model of taxation could push the online gaming industry towards unregulated grey markets. Discuss. (150 words) |

The Court treated the 2023 GST amendments as "clarificatory" in nature. Because they merely clarified the existing legal position on taxing actionable claims, the government is allowed to apply the tax notices for periods prior to October 2023.

In the Gross Gaming Revenue (GGR) model, tax is levied only on the commission or "rake fee" retained by the platform. In the turnover model, the tax is applied to the entire deposit or full face value of the bet placed by the player, significantly increasing the tax burden.

The Supreme Court clarified that for GST purposes, if players stake money on uncertain outcomes, the activity falls under betting or gambling. This effectively blurred the tax-protection shield previously offered by the "skill versus chance" distinction.

© 2026 iasgyan. All right reserved