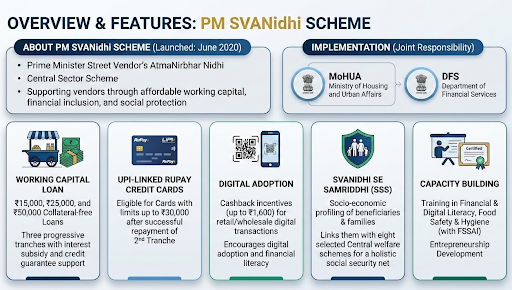

The PM SVANidhi scheme empowers street vendors by providing collateral-free working capital loans, interest subsidies, and digital cashback incentives. Recently extended to 2030, it fosters financial inclusion, digital adoption, and socio-economic welfare through the SVANidhi se Samriddhi initiative.

The PM SVANidhi scheme completed six years of operations and has been restructured and extended till March 31, 2030.

The Pradhan Mantri Street Vendor’s AtmaNirbhar Nidhi (PM SVANidhi) is an urban micro-credit intervention launched by the Ministry of Housing and Urban Affairs (MoHUA) in 2020.

Initially conceived as an emergency life support system during the COVID-19 pandemic, it has evolved into a permanent institutional platform for financial inclusion and socio-economic empowerment for the informal economy.

It is a Central Sector Scheme providing collateral-free working capital loans to urban street vendors.

Credit disbursement occurs through Scheduled Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks (SFBs), Cooperative Banks, Non-Banking Financial Companies (NBFCs), and Microfinance Institutions (MFIs).

The Department of Financial Services (DFS) oversees the various banking and financial institutions (such as SIDBI and public sector banks like PNB and SBI) that facilitate the scheme's delivery.

Expansion: The Government restructured and extended the scheme until March 31, 2030, with a revised financial outlay of ₹7,332 crore.

Objectives of PM SVANidhi

Formal Credit Access: Dismantle barriers to institutional credit for micro-entrepreneurs who historically relied on high-interest informal moneylenders.

Financial Inclusion: Reintegrate the "bottom of the pyramid" into the formal banking system, enabling them to build official credit scores for the first time.

Digital Transformation: Incentivize the adoption of digital payment mechanisms (UPI) among roadside stalls to drive the digital economy.

Socio-Economic Upliftment: Provide a holistic safety net for vendors and their families through linkages to other government welfare schemes.

Business Sustainability: Strengthen the resilience and earning capacity of the informal workforce to contribute to the Viksit Bharat 2047 agenda.

Key Features of PM SVANidhi

Three-Tier Progressive Lending Model

The scheme operates a "progressive lending ladder" to reward fiscal discipline and timely repayment:

|

Tranche |

Loan Amount (Standard) |

Revised/Enhanced Amount (Post-Aug 2025) |

Repayment Tenure |

|

1st Tranche |

Up to ₹10,000 |

Up to ₹15,000 |

6 to 12 months |

|

2nd Tranche |

Up to ₹20,000 |

Up to ₹25,000 |

6 to 18 months |

|

3rd Tranche |

Up to ₹50,000 |

Up to ₹50,000 |

Up to 36 months |

Financial Incentives

SVANidhi se Samriddhi (SSS)

Multi-Level Monitoring Framework

The scheme employs a rigorous oversight structure to ensure delivery:

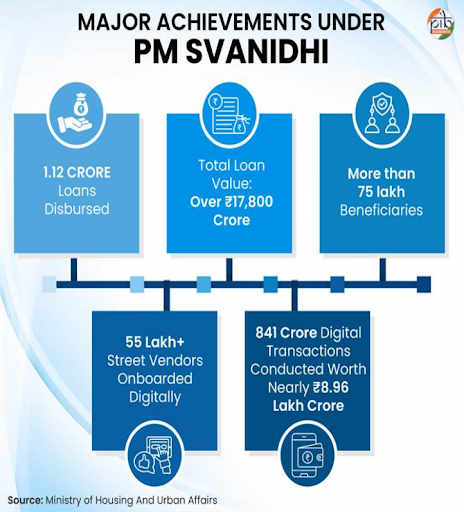

Massive Scale: As of March 1, 2026, the scheme disbursed 1.12 crore loans totaling ₹17,800 crore to over 75 lakh beneficiaries.

Banking First: Impact studies by the Indian School of Business (ISB) reveal that 95% of beneficiaries accessed their first-ever bank loan through this scheme.

Digital Reach: Over 55 lakh vendors are digitally onboarded, recording 841 crore transactions worth approximately ₹9 lakh crore.

Economic Gains: Beneficiary incomes recorded an average annual increase of nearly 20%.

Credit Graduation: Approximately 30% of borrowers successfully accessed formal credit products outside PM SVANidhi, indicating a genuine "graduation" effect.

Social Equity:

Recognition: The scheme received the Prime Minister’s Award for Excellence in Public Administration for Innovation.

Digital Literacy Gap: Persistent deficits in digital literacy and smartphone penetration, particularly in smaller Urban Local Bodies (ULBs) and Municipal Committees.

Information Asymmetry: Significant gaps in scheme awareness remain among vendors despite measurable penetration.

Technical Hurdles: Issues such as failure to receive OTPs and app-based stability problems hinder the application process.

Geographic Variation: Larger urban bases (e.g., Punjab with 167 ULBs) show higher absolute volumes, while smaller states or towns struggle with sanctioned-to-disbursed conversion rates.

Inadequate Infrastructure: Restricted banking correspondent networks in peri-urban areas impede cashback uptake and UPI adoption.

Geographic Expansion: Extend coverage beyond statutory towns to include census towns and peri-urban areas in a graded manner.

Institutional Replication: Replicate high-performance models, such as Haryana's pilot-town framework (Karnal, Hisar, Ambala), across all non-pilot ULBs to improve conversion efficiency.

Credit Ceiling Revision: Progressively revise credit limits to align with inflationary trends and evolving business requirements.

Targeted Digital Literacy: Direct investments toward digital financial literacy initiatives in district-level civic bodies where digitalization lags behind major Municipal Corporations.

Simplified Documentation: Enforce strict application timelines and simplify KYC procedures to reduce the sanction-to-disbursement lag.

PM SVANidhi fosters self-reliance among millions of informal vendors by integrating them into the formal economy through tech-driven governance and institutional financial inclusion.

Source: PIB

|

PRACTICE QUESTION Q. Consider the following statements regarding the PM SVANidhi scheme:

Which of the statements given above are correct? A) 1 and 2 only B) 2 and 3 only C) 1 and 3 only D) 1, 2, and 3 Answer: D Explanation: Statement 1 is correct: The scheme provides collateral-free working capital loans in three progressive tranches. While the initial tranche limits were ₹10,000 and ₹20,000, they have been enhanced (to ₹15,000 and ₹25,000 respectively in the restructured scheme), but the third tranche remains ₹50,000. Thus, the loans are provided up to ₹50,000. Statement 2 is correct: Beneficiaries are eligible for an interest subvention of 7% per annum on timely or early repayment of the loan. This subsidy is credited quarterly via Direct Benefit Transfer (DBT). Statement 3 is correct: The lending period of the scheme, initially valid until March 2022 and later December 2024, has been extended until March 31, 2030. |

The PM SVANidhi (Pradhan Mantri Street Vendor's AtmaNirbhar Nidhi) scheme is a central micro-credit initiative launched in June 2020 to provide collateral-free working capital loans to urban street vendors whose livelihoods were affected by the COVID-19 pandemic.

Under the restructured scheme, loans are provided in three progressive tranches: up to ₹15,000 for the first tranche, up to ₹25,000 for the second tranche, and up to ₹50,000 for the third tranche.

It is an added initiative that conducts socio-economic profiling of vendors and their families, facilitating their access to eight central welfare schemes, including PM Jeevan Jyoti Bima Yojana and PM Suraksha Bima Yojana.

© 2026 iasgyan. All right reserved