India Post Payments Bank (IPPB) successfully converted India's vast postal network into a digital banking system, democratizing financial access for rural citizens and women. While profitable, its future success requires evolving products and adapting to regulatory and technological changes.

Why In News?

The India Post Payments Bank (IPPB) launched a dedicated Self Help Group (SHG) Savings Account to advance financial inclusion and empower women-led SHGs across rural India.

What is India Post Payments Bank (IPPB)?

It is a state-owned payments bank established under the Department of Posts, Ministry of Communications, with 100% equity owned by the Government of India.

It was initially launched as a pilot project in 2017, and in 2018 expanded nationwide to build an accessible, affordable, and trusted bank for the common citizen.

Its fundamental mandate is to promote financial inclusion by removing barriers for unbanked and underbanked populations.

|

Payments banks were established based on the recommendations of the Dr. Nachiket Mor Committee in 2013-2014, aimed at boosting financial inclusion for low-income households, small businesses, and migrant labor. |

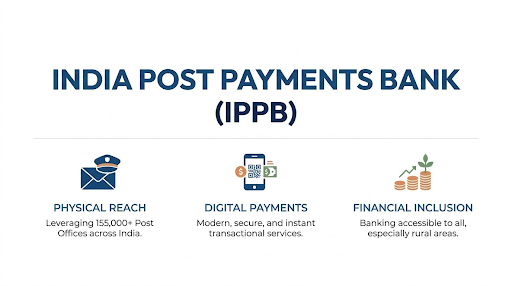

IPPB operates on a physical-digital hybrid model, to leverage the country's vast postal infrastructure, utilizing over 1.5 lakh post offices.

Operating under the motto "Aapka Bank, Aapke Dwaar," it empowers postmen and Gramin Dak Sevaks to act as financial advisors providing last-mile doorstep banking.

As a payments bank, it operates under a differentiated regulatory model where it can accept deposits and facilitate remittances, but it is strictly prohibited from lending money directly.

Savings and Current Accounts: IPPB offers Basic, Regular, DigiSmart, and SHG accounts with a ₹2 lakh balance limit.

Doorstep Banking: Citizens can open accounts, transfer funds, deposit or withdraw cash, and pay bills from the comfort of their homes using the local postman, often at nil or nominal charges.

Direct Benefit Transfers (DBT): Bank acts as a secure electronic channel to route government subsidies, scholarships, and pensions (like PM Kisan and LPG subsidies) directly into citizens' Aadhaar-linked accounts.

Aadhaar Enabled Payment System (AePS): Allows citizens to access their Aadhaar-linked accounts held with other banks for cash withdrawals, balance inquiries, and mini statements through the postman.

Ancillary Services: IPPB facilitates utility bill payments, domestic money transfers, mobile updates in Aadhaar, generation of Digital Life Certificates (Jeevan Pramaan), and third-party products like life and general insurance.

Massive Customer Outreach: IPPB has successfully opened over 13 crore accounts, of which 77% are rural accounts and 48% are held by women. (Source: Ministry of Communications)

High Transaction Volume: In the 2024-25 financial year, IPPB recorded over 680 crore total transactions with transaction value of over Rs 6 lakh Crore. (Source: Ministry of Communications)

Driving Financial Inclusion: Bank has disbursed over ₹7 Lakh Crore in Direct Benefit Transfers, empowering rural households and ensuring leak-proof welfare distribution.

Financial Profitability: Overcoming early deficits, IPPB achieved financial viability in its fifth year of operation (2022-23) and reported a net profit of ₹25 Crore for the 2023-24 financial year.

Regulatory Restrictions: RBI's strict prohibition on lending restricts IPPB's ability to diversify its revenue streams, keeping it heavily dependent on transaction fees and commissions.

High Operational Costs: Reaching the rural last mile involves high physical outreach and compliance costs that lean, digital-only private competitors do not bear.

Market Competition: Digital payments landscape in India is highly competitive, dominated by UPI-based fintechs (such as Google Pay and PhonePe) and other payments banks that focus on highly profitable urban remittances.

Cybersecurity Vulnerabilities: Rapid onboarding of previously unbanked, digitally inexperienced rural populations exposes the bank and its customers to evolving fraud and cybersecurity risks.

Service Diversification: IPPB should expand its offerings into higher-margin areas like micro-pensions, investment advisory, and broader insurance distribution.

Policy Reform: RBI could grant IPPB limited lending rights under strict regulatory safeguards to boost its revenue.

Technology Leverage: Adopting advanced technologies like AI and blockchain can enhance real-time monitoring, reduce costs, and improve fraud detection.

Cost Rationalization: IPPB needs to optimize training for postal workforce and create incentives that push customers toward low-cost, digital-first transactions.

India Post Payments Bank (IPPB) successfully leveraged its vast postal network to democratize digital financial access and achieve profitability, but its long-term viability depends on continuous product innovation, cost optimization, and adaptation to regulatory and technological shifts.

Source: PIB

|

PRACTICE QUESTION Q. With reference to the India Post Payments Bank (IPPB), consider the following statements: 1. It was established based on the recommendations of the Urjit Patel Committee. 2. It is legally permitted to issue credit cards but cannot issue loans. 3. It must invest at least 75% of its demand deposit balances in risk-free Government Securities (G-Secs). Which of the statements given above is/are correct? a) 1 and 2 only b) 3 only c) 2 and 3 only d) 1, 2, and 3 Answer: b) 3 only Explanation: Statement 1 is Incorrect: The Nachiket Mor Committee (Committee on Comprehensive Financial Services for Small Business and Low Income Households) recommended the establishment of Payments Banks in 2014. Statement 2 is Incorrect: Payments Banks are not permitted to issue credit cards. They can issue ATM/debit cards but are strictly prohibited from undertaking lending activities or issuing credit cards. Statement 3 is Correct: To ensure the safety of deposits, Payments Banks are statutorily required to invest at least 75% of their "demand deposit balances" in Government Securities (G-Secs) or Treasury Bills with a maturity of up to one year. The remaining 25% must be held in current and time deposits with other scheduled commercial banks for operational liquidity. |

IPPB is a 100% government-owned banking entity under the Department of Posts. Conceptualized on the recommendations of the Nachiket Mor Committee, it leverages India's vast postal infrastructure to provide specialized savings, digital banking, and remittance services primarily to rural and low-income populations.

Unlike traditional commercial banks, IPPB operates under a differentiated regulatory framework. The Reserve Bank of India (RBI) strictly prohibits payments banks from lending money or issuing credit cards. IPPB can only accept deposits up to a limit of ₹2,00,000 per customer and must invest at least 75% of its demand deposits in government securities.

Citizens can access interoperable doorstep banking, including opening paperless accounts, cash deposits, and withdrawals. They can also access Aadhaar Enabled Payment System (AePS) services, receive Direct Benefit Transfers (DBT) directly into their accounts, update Aadhaar details, pay utility bills, and generate Digital Life Certificates (Jeevan Pramaan).

© 2026 iasgyan. All right reserved