Small Savings Schemes (SSS) are government-backed instruments like PPF, SSY, and NSC, designed to encourage household savings. They offer sovereign guarantees, competitive interest rates, and tax benefits, providing financial security while mobilizing resources for nation-building and infrastructure development.

The government on Monday kept interest rates unchanged for various small savings schemes, including PPF and NSC, for the eighth consecutive quarter starting April 1, 2026.

Small Savings Schemes (SSS) are government-backed, secure investment instruments in India, managed via the National Small Savings Fund (NSSF) and India Post

The National Small Savings Fund (NSSF), established in 1999 within the Public Account of India.

Fund Flow: All deposits from small savings schemes are credited to the NSSF. All withdrawals and interest payments are debited from it.

Investment Pattern: The net collections in the NSSF are invested in Central and State Government Securities (G-Secs). This makes small savings a "non-market" source of internal borrowing for the government.

Fiscal Impact: While these funds help finance the fiscal deficit, they are technically "liabilities" of the Public Account. This allows the government to borrow without immediately impacting the market yields of G-Secs.

Post Office Deposits (Liquid Savings)

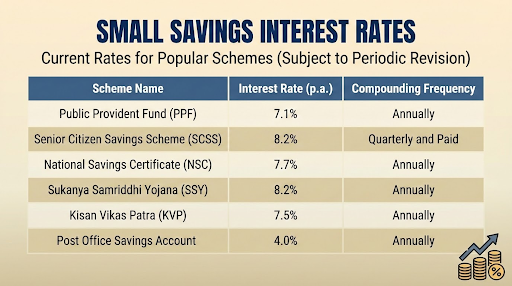

Post Office Savings Account: Similar to a commercial bank savings account, offering a modest interest rate (currently 4.0%).

Time Deposits (TD): Fixed deposits available for tenures of 1, 2, 3, and 5 years.

Recurring Deposits (RD): A 5-year systematic investment plan designed for small monthly contributions.

Monthly Income Account (MIS): Provides a fixed monthly payout.

Savings Certificates (Capital Accumulation)

National Savings Certificate (NSC): A 5-year instrument popular among salaried employees for tax deductions under Section 80C.

Kisan Vikas Patra (KVP): Initially designed for farmers but now open to all; it doubles the principal amount over a predefined period (currently approx. 115 months).

Social Security Schemes (Long-term Welfare)

Public Provident Fund (PPF): A 15-year statutory scheme with "EEE" (Exempt-Exempt-Exempt) tax status. It is the primary retirement tool for the unorganized sector.

Sukanya Samriddhi Yojana (SSY): Part of the Beti Bachao Beti Padhao campaign, offering high interest rates for the education and marriage of the girl child.

Senior Citizens Savings Scheme (SCSS): For those aged 60+, offering quarterly interest payouts.

Resource Mobilization: SSS provides a steady stream of domestic capital, reducing India's reliance on volatile external debt and helping maintain a stable Current Account.

Promoting Financial Inclusion: With the vast network of 1.5 lakh+ Post Offices, these schemes reach "The Last Mile" where formal banking presence is thin.

Real Interest Rates: During periods of moderate inflation, these schemes provide "Real Positive Interest Rates," protecting the purchasing power of the middle class and senior citizens

Hindrance to Monetary Policy Transmission

The "Floor" Effect: Small savings rates are higher than bank deposit rates. This creates a floor below which banks cannot lower their deposit rates without losing customers to post offices.

Impact on Lending: If banks cannot lower deposit rates, they cannot reduce their MCLR (Marginal Cost of Funds Based Lending Rate). This hinders the RBI’s ability to transmit repo rate cuts to the broader economy.

High Fiscal Cost of Borrowing

Expensive Debt: Borrowing from the National Small Savings Fund (NSSF) is 50–100 basis points more expensive for the government than issuing Government Securities (G-Secs) in the open market. (Source: 15th Finance Commission Report)

Diversion of Funds: Heavy reliance on NSSF for financing the fiscal deficit can lead to a lack of fiscal discipline, as these are "off-budget" liabilities in the Public Account.

Distortions in the Savings

Taxation Inconsistencies: The coexistence of EEE (Exempt-Exempt-Exempt) schemes like PPF and fully taxable schemes like Senior Citizen Savings Scheme (SCSS) creates an uneven playing field, often benefiting higher-income tax-savers over the truly "small" savers.

Gender and Age Gaps: While schemes like Sukanya Samriddhi (SSY) are successful, rural women still face barriers in accessing these schemes due to a lack of digital literacy and documentation.

Full Market Linkage

Implementing Gopinath Committee Norms: The government should move toward a strict quarterly adjustment of SSS rates based on the previous quarter's G-Sec yields to ensure that SSS rates do not remain artificially high when market rates are falling.

Rationalization of Tax Benefits

Moving toward EET/TTE: Shifting long-term savings toward the EET (Exempt-Exempt-Taxed) model, similar to the National Pension System (NPS), would bring uniformity and reduce the fiscal burden of tax foregone.

Digital Integration & Financial Literacy

Post Office-Bank Interoperability: Enhancing the Core Banking Solution (CBS) in all 1.5 lakh+ post offices to allow seamless transfers between post office savings and commercial bank accounts.

Targeted Awareness: Using Common Service Centres (CSCs) to promote the SSY in aspirational districts.

Balancing Social Security with Efficiency

Protecting Vulnerable Segments: While general rates (like Time Deposits) should be market-linked, the government should continue providing a protected spread for Senior Citizens (SCSS) and the Girl Child (SSY) to maintain the social safety net.

Small Savings Schemes act as a vital bridge between financial inclusion for citizens and a reliable source of low-cost capital for the government's developmental projects.

Source: MONEYCONTROL

|

PRACTICE QUESTION Q. Consider the following statements regarding the National Small Savings Fund (NSSF): 1. It was established within the Consolidated Fund of India. 2. The net collections in the NSSF are primarily invested in Central and State Government Securities. Which of the statements given above is/are correct? (a) 1 only (b) 2 only (c) Both 1 and 2 (d) Neither 1 nor 2 Answer: (b) Explanation: Statement 1 is Incorrect: The National Small Savings Fund (NSSF) was established in 1999, but it is maintained within the Public Account of India, not the Consolidated Fund of India. According to Article 266(2) of the Constitution, the Public Account is for moneys received by or on behalf of the Government of India that are not part of the Consolidated Fund. Small savings are considered "liabilities" of the government because they must be repaid to the depositors with interest. Statement 2 is Correct: The net collections (deposits minus withdrawals) in the NSSF are invested in Special Central and State Government Securities. This mechanism allows the NSSF to act as a crucial source of internal, non-market borrowing for both the Union and State governments to finance their fiscal deficits. |

The NSSF was established by the Government of India in 1999 to pool all money collected through various small savings instruments (like PPF, NSC, and Post Office Deposits). It acts as a captive source of internal borrowing for the government to finance its fiscal deficit.

Based on the recommendations of the Shyamala Gopinath Committee (2011), the interest rates of Small Savings Schemes are benchmarked to the secondary market yields of Government Securities (G-Secs) of comparable maturity. The Ministry of Finance revises these rates quarterly.

When the RBI cuts the Repo Rate to lower borrowing costs, commercial banks struggle to reduce their deposit rates because they must compete with the high, government-backed interest rates of Small Savings Schemes (like PPF or SCSS). Consequently, banks keep lending rates high, hampering credit flow to sectors like MSMEs and real estate.

© 2026 iasgyan. All right reserved