Description

Disclaimer: Copyright infringement not intended.

Context

- SEBI just gave the green light for same-day settlement (T+0) for 25 stocks and a few brokers.

Settlement Cycle

- A settlement cycle refers to the time period between the execution of a trade in the securities market and the exchange of funds and securities.

- A shorter settlement cycle reduces the time gap between trade execution and settlement, thereby mitigating counterparty risk, market risk, and liquidity risk for market participants.

- It also facilitates the efficient utilization of capital and enhances market turnover and efficiency.

Practice in India

- Over the years, the Indian securities market has witnessed a gradual reduction in settlement cycles.

- In 2002, the settlement cycle was shortened from T+5 (five days after trade) to T+3, and further reduced to T+2 in 2003.

- In 2021, SEBI introduced the T+1 settlement cycle, which was fully implemented from January 2023, making India the second nation to introduce a shorter cycle. Currently, India follows a T+1 settlement cycle for the equity cash segment, meaning that trades are settled on the next working day after the trade date.

International Practices

- Globally, China has already transitioned to shorter settlement cycles such as T+0 or same-day settlement. Some countries, including the United States, United Kingdom and Singapore and Japan follow either T+1 or T+2 settlement cycle.

- Moreover, there are initiatives to introduce instant or real-time settlement in certain markets, for instance, the Depository Trust and Clearing Corporation’s Project Ion in the United States, which leverages distributed ledger technology for instant settlement of trades.

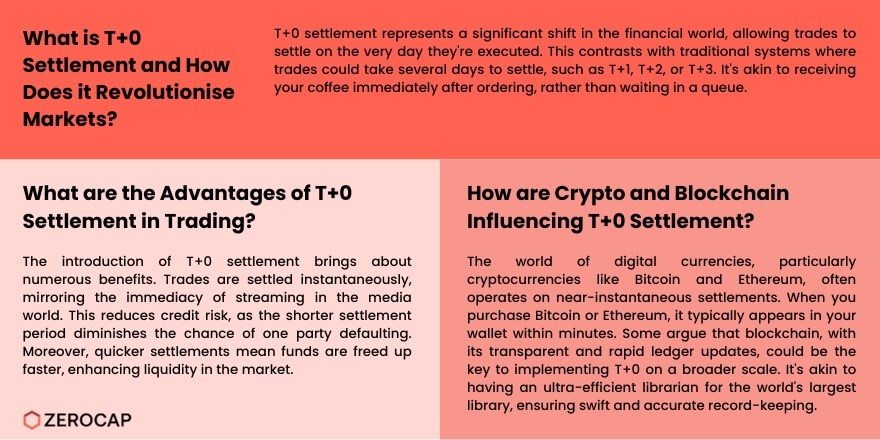

What is the T+0 settlement?

- The market regulator's proposal is to settle trades on the same day in the stock market for immediate transfer of funds and securities between buyers and sellers. In the T+0 settlement, investors selling their stocks will receive money on the day of the sale instead of the current T+1 process, in which the trades are settled on the next trade day.

- To simplify, after an investor sells their shares in the stock market, they receive money in their demat accounts on the next trading day. In the T+0 programme, the money will be credited on the same day of sale.

How will T+0 settlement be implemented?

- SEBI has proposed that the new settlement process will be implemented in two phases. In the first phase, an optional T+0 settlement cycle is proposed for trades until 1:30 pm, with the settlement of funds and securities to be completed on the same day by 4:30 pm.

- In the second phase, an optional immediate trade-by-trade settlement for funds and securities will be introduced, allowing trading until 3:30 pm. After this phase is implemented, Phase 1 (optional T+0 settlement) will be discontinued.

How will it work?

- SEBI chairperson Madhabi Puri Buch said that the T+0 settlement will be an optional parallel process applicable to non-custodian or non-institutional clients.

- Initially, T+0 settlements will be made available for the top 500 listed equity shares based on market capitalisation. This will be done in three tranches of 200, 200, and 100, starting from the lowest and moving towards the highest market cap.

- Experts believe that shortening the settlement cycle will increase liquidity in the market because it will ensure faster access to cash, enabling more money to flow into the market and making it more liquid.

Implications for Stakeholders

Investors:

- Benefit from greater flexibility and choice.

- Can tailor settlement preferences based on risk appetite and funding availability.

- Advantages include faster pay-out of funds and securities.

- Challenges include higher funding costs and operational complexity.

Intermediaries:

- Face operational, technological, and regulatory challenges.

- Need to upgrade systems and ensure compliance with legal and regulatory changes.

- Manage increased funding and liquidity requirements.

Regulators and Market Infrastructure Institutions:

- Have a pivotal role in implementing and overseeing the proposed settlement cycles.

- Ensure smooth implementation and monitor impact.

- Provide guidance and support to market participants.

- Navigating Feasibility and Mitigating Strategies

Feasibility Analysis:

- Assess cost-benefit dynamics and risk-reward trade-offs.

- Consider readiness of market participants and infrastructure.

.jpg)

Mitigation Measures:

- Address impact of taxation and stamp duty.

- Streamline corporate actions and investor entitlements.

- Optimize margin and collateral requirements.

- Simplify dispute resolution mechanisms.

Conclusion and Way Forward

- SEBI presents a forward-thinking initiative to introduce optional T+0 and instant settlement, aligning with global best Q.practices. While offering benefits like enhanced market efficiency, liquidity, and safety, it requires addressing operational, technological, and regulatory challenges. A comprehensive approach involving gradual implementation, monitoring, and periodic reviews is essential for success and to realize the potential benefits for the Indian securities market.

|

What is a rolling settlement?

Rolling settlement refers to the process whereby security trades are settled on a rolling basis instead of on a fixed date. In this setup, securities traded on the current date are settled on successive dates. In July 2001, SEBI introduced the rolling settlement system, replacing the fixed settlement cycle, which was blamed for poor delivery, distrust among traders, and frequent defaults. By December 20021, all listed companies started following a T+5 settlement (5 business days from the trade date) cycle. Eventually, the settlement cycle was reduced to T+3 in April 2002 and further to T+2 in April 2003.

In September 2021, the SEBI allowed stock exchanges to introduce a T+1 settlement cycle on any of the securities available in the equity segment starting January 1, 2022. With the huge inflow of equity investors in recent years, the market regulator's new settlement process is expected to benefit traders.

|

|

PRACTICE QUESTION

Q. Which of the following statements accurately describes the characteristic feature of a rolling settlement in asset trading?

A) Trades completed on any given day are settled on the same day.

B) Settlement dates for trades depend on the specific date when the trade was executed.

C) All trades are settled on a fixed date after the trade date, regardless of when they were initiated.

D) Trades are settled periodically, typically every month, regardless of the trade date.

Choose the correct option:

1.A

2.B

3.C

4.D

Answer 2. B)

|