Payments Banks are specialized "niche" banks introduced by RBI to promote financial inclusion. They accept demand deposits up to ₹2 lakh, issue debit cards, and facilitate remittances, but are strictly prohibited from lending money or issuing credit cards.

The Reserve Bank of India (RBI) cancelled the banking license of Paytm Payments Bank Limited (PPBL) on April 24, 2026, directing the bank to cease operations immediately.

Based on the recommendations of the Nachiket Mor Committee, RBI introduced Payments Banks as a specialized "niche" banking model to promote financial inclusion.

Unlike traditional universal banks (like SBI or HDFC), Payments Banks are "differentiated" banks because they operate with specific restrictions to protect small depositors and minimize risk.

Objectives

Payments Banks provide small savings accounts and payments/remittance services to:

What They CAN Do (Permissible Activities)

Accept Deposits: Can accept demand deposits (savings and current accounts) up to a limit of ₹2 lakh per individual customer.

Issue Cards: Can issue ATM/Debit cards

Payments & Remittances: Can facilitate transactions through various channels like UPI, IMPS, and NEFT.

Distribution Services: Can distribute non-risk sharing simple financial products like mutual funds and insurance.

What They CANNOT Do (Restrictions)

No Lending: Strictly prohibited from lending money or providing loans.

No Credit Cards: Cannot lend, cannot issue credit cards.

No NRI Deposits: Cannot accept deposits from Non-Resident Indians (NRIs).

Investment Restrictions: Cannot set up subsidiaries to undertake non-banking financial services.

Key Regulatory Requirements

Minimum Capital: The minimum paid-up equity capital for payments banks is ₹100 crore.

Statutory Liquidity Ratio (SLR): They must invest a minimum of 75% of their "demand deposit balances" in Government Securities/Treasury Bills with a maturity of up to one year.

CRR Compliance: They must maintain the Cash Reserve Ratio (CRR) with the RBI just like regular banks.

Current Status

As of early 2026, major players in this sector included Airtel Payments Bank, India Post Payments Bank (IPPB), and Jio Payments Bank.

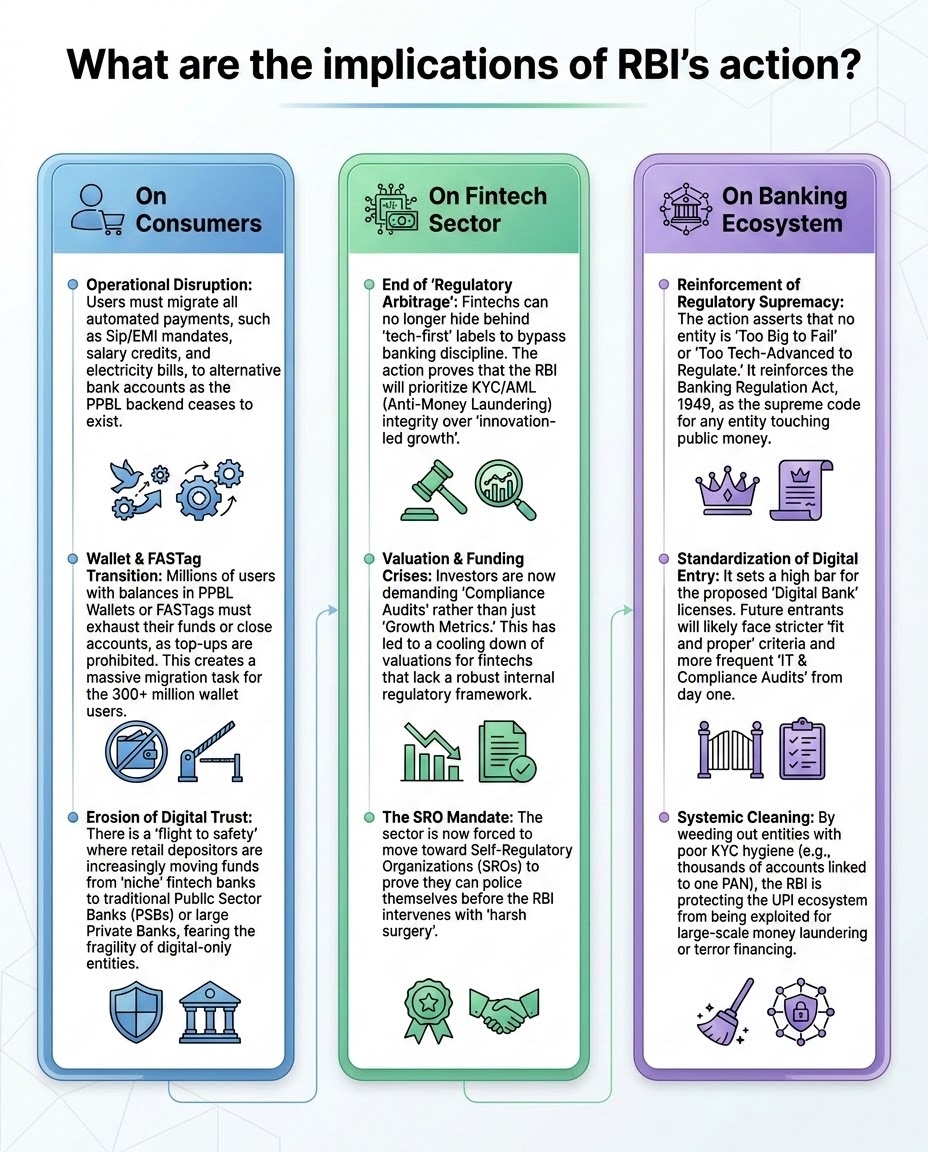

Detrimental Operations: The RBI stated PPBL operated in a manner harmful to the interests of the bank and its depositors.

KYC & Money Laundering: Discovery of single PANs linked to thousands of accounts signaled a breakdown in KYC protocols and posed severe money laundering risks.

Governance Failures: The bank lacked independence from its parent Company, and management practices were deemed prejudicial to public interest.

Repeated Violations: Despite 2022 onboarding bans and 2024 warnings, persistent non-compliance led to the final license revocation in April 2026.

Source: THE HINDU

Source: THE HINDU

|

PRACTICE QUESTION Q. Which of the following activities is a Payments Bank permitted to undertake?

Select the correct answer using the code below: (a) 1 and 2 only (b) 1 and 3 only (c) 1, 2, and 3 (d) 2, 3, and 4 Answer: B Explanation: Statement 1 is Correct: According to RBI guidelines, Payments Banks are permitted to accept demand deposits (savings and current accounts). The initial limit of ₹1 lakh per individual customer was revised to ₹2 lakh in 2021. Statement 2 is Incorrect: Payments Banks are strictly prohibited from issuing credit cards because they are not allowed to undertake credit risk. They can, however, issue ATM and debit cards. Statement 3 is Correct: Payments Banks are allowed to undertake non-risk sharing of simple financial services, including the distribution of third-party products like mutual funds and insurance policies. Statement 4 is Incorrect: A fundamental restriction on Payments Banks is that they cannot engage in any lending activities. This includes agricultural loans, personal loans, or any other form of credit. |

Payments Banks are a differentiated category of banks conceptualized to advance financial inclusion. They provide secure, technology-driven payment and remittance services to unbanked and underbanked sectors, including low-income households, migrant laborers, and small businesses.

As per the enhanced RBI guidelines in 2021, Payments Banks can accept demand deposits (both savings and current accounts) up to a maximum limit of ₹2 lakh per individual customer.

The RBI cited persistent non-compliance and continued material supervisory concerns. Issues included a failure to maintain a regulatory arm's-length distance from its parent tech company, flawed corporate governance, and severe KYC/anti-money laundering violations identified by the FIU-IND.

© 2026 iasgyan. All right reserved