India’s Q2 FY26 GDP growth of 8.2% reflects strong momentum in manufacturing, services and corporate profitability, supported by policy-driven public investment. However, the weak nominal GDP growth, low GDP deflator, slowing agriculture, soft rural demand and subdued private investment reveal underlying structural pressures. These trends raise concerns about fiscal space, data reliability and the durability of the recovery, highlighting the need for broader demand strengthening, rural income support, and revival of private capital formation to ensure sustainable and inclusive growth.

Copyright infringement not intended

Picture Courtesy: The Hindu

India’s GDP growth accelerated to 8.2% in Q2 FY26, the highest in six quarters. While the headline real growth appears robust, the nominal GDP growth of only 8.7% highlights deeper structural concerns.

|

Must Read: GDP | INDIA'S $30TRILLION ECONOMY BY 2025: PROJECTIONS, CHALLENGES & OPPORTUNITIES | REVISION OF GDP METHODOLOGY | |

|

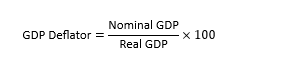

BASIC CONCEPTS GDP (Gross Domestic Product) Nominal GDP Definition: Nominal GDP is the value of final goods and services measured at current prices of the same year. Includes inflation or price changes. Formula: If India produces 100 units and each cost ₹100 this year: If next year prices rise to ₹120 (inflation), nominal GDP becomes: Real GDP Real GDP is the value of final goods and services measured at constant prices (base-year prices). Excludes inflation. Formula: Example: Using the above numbers: GDP Deflator Since Nominal vs Real GDP differ by price changes, the link between them is the: GDP Deflator = Measure of inflation for the whole economy

If deflator is low → nominal GDP is low → real GDP looks higher.

|

Manufacturing Resurgence (9.1%): Aided by double-digit corporate profit growth, lower commodity prices, and productivity improvements. Boosted by low base effect (2.1%).

Services Sector Momentum (9.2%): Financial, real estate & professional services saw a nine-quarter high (10.2%). Public administration and defence expanded at 9.7%, even as central non-interest expenditure contracted.

Agriculture Slowdown (3.5%): Reflects monsoon variability, rural distress, and stagnating productivity. Reinforces concerns about rural demand recovery.

Nominal GDP reflects the economy’s value in monetary terms, combining both real activity and the prevailing price level. When nominal GDP grows slowly despite high real GDP numbers, it signals that prices in the economy are barely rising, or in some pockets, even stagnating.

Nominal GDP represents the economy’s financial strength: A slowing nominal GDP implies that the overall value of goods and services, when expressed in rupees, is not expanding rapidly.

These matters because:

A very low GDP deflator points to deeper structural softness: The GDP deflator is the broadest measure of price changes in the economy. When the deflator is unusually low:

Weak nominal growth suggests suppressed pricing power: In a healthy economy, rising incomes and robust demand allow firms to raise prices moderately.

When nominal GDP slows sharply:

This reflects an economy generating output without commensurate income growth, which is unsustainable for long-term development.

Private Consumption Gathers Pace

Private Final Consumption Expenditure (PFCE) expanded by 7.9%, improving from 7% in the previous quarter. This pick-up in consumption is linked to:

Economists point out that lower inflation created room for households to spend more on non-essential items, strengthening the consumption-led recovery.

Investment Activity Supported Mainly by Public Capex

Gross Fixed Capital Formation (GFCF) rose 7.3%, largely supported by:

However, analysts caution that private investment is still navigating global uncertainties, including elevated U.S. tariffs and external demand risks.

Positive Signals:

Manufacturing and services are carrying the recovery: Manufacturing grew 9.1%, the highest in six quarters. Services expanded 9.2%, with financial and professional services touching 10.2%, the fastest in nine quarters. These two sectors account for ~75% of GDP and their strong performance indicate rising urban demand, corporate sector efficiency gains and support from government capex

Corporate Profitability Remains Robust: Listed companies recorded ~17–20% profit growth in Q2 (NSE-500 average). Operating margins improved due to lower input costs (metals, energy). High profitability supports steady tax collections (corporate tax is 28% of India’s gross tax revenue), reinvestment capacity and resilience to global shocks

Policy Stability Boosts Investment Climate: India’s macro framework focus on public capex, digital governance, tax reforms, and PLI schemes has created predictability for investors. Government capital expenditure rose 31% Year on Year. FDI approvals in PLI-linked sectors increased 9–10%. This stable policy environment underpins medium-term investment confidence.

Negative Signals:

Weak Nominal GDP Signals Soft Demand: Nominal GDP grew only 8.7%, far below the budget assumption of 10.1%. GDP deflator is around 0.5%, not aligned with CPI inflation (~4–5% range). Nominal GDP drives tax revenues, fiscal deficit ratios, corporate turnover and wage and income valuations

Agriculture Slowdown & Rural Demand Stress: Agriculture grew only 3.5%, down from 4.1% last year. Rural wage growth is stagnant at ~1–2% real terms. Food inflation continues to hurt household budgets.

Private Investment Still Below Take-off Point: GFCF grew 7.3%, largely due to government capex, not private investment. Private capex announcements (CMIE data) remain 25% below pre-pandemic levels. Without strong private-sector investment, long-term growth may plateau around 6.5–7%, as capacity addition slows, job creation moderates, and innovation cycles weaken.

India’s six-quarter-high GDP growth reflects genuine momentum in manufacturing, services and corporate performance, but the weak nominal GDP, rural stress, subdued private investment and data credibility concerns reveal underlying fragilities. Sustaining growth will depend on strengthening rural incomes, restoring private investment confidence, and improving statistical transparency so that headline expansion translates into broad-based and durable economic well-being.

Source: The Hindu

|

Practice Question Q. India’s strong real GDP growth in Q2 FY26 coexists with weak nominal GDP and sectoral stress. Discuss (150 words) |

Nominal GDP reflects the monetary value of economic activity. When nominal growth is low, tax revenues fall short, fiscal deficit ratios worsen, and corporate turnover slows. This weakens the overall financial strength of the economy, even if real output is rising.

It suggests that official price growth is far below what households and firms are experiencing. A low deflator inflates real GDP artificially and may indicate weak pricing power, subdued demand, or statistical gaps in capturing inflation.

Rural India accounts for nearly 35–40% of total consumption. When agriculture slows and rural incomes stagnate, demand in FMCG, two-wheelers, garments, and low-value services weakens, dragging down the broader consumption recovery.

© 2026 iasgyan. All right reserved