The Central Bank Digital Currency (CBDC) pilot marks a shift toward sovereign digital fiat, offering efficient targeted welfare and settlements. While promising, the RBI must address privacy concerns and cybersecurity through holding limits and legislative safeguards to ensure a resilient digital economy.

The Central Bank Digital Currency (CBDC) pilot has exceeded 150 million transactions with a value surpassing ₹34,000 crore.

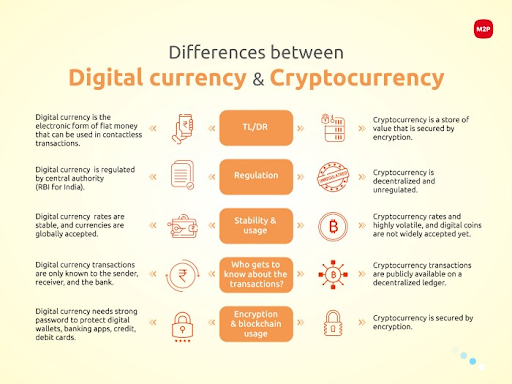

A CBDC is the digital form of a country's official fiat currency.

Types of CBDCs

Retail CBDC (e₹-R): For public use in everyday transactions by individuals and businesses. It can be:

Wholesale CBDC (e₹-W): For use by financial institutions only, to settle large interbank transfers and securities transactions efficiently.

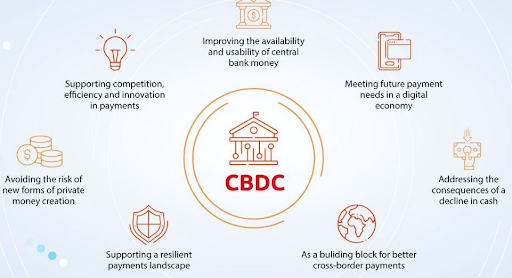

Financial Inclusion & Targeted Welfare: CBDCs can be "programmed" for specific uses.

Reduced Currency Management Costs: Central banks can cut down on the high costs associated with printing, distributing, and managing physical currency.

Efficient Cross-Border Payments: Platforms like Project mBridge enable direct, instantaneous settlements between countries, bypassing the slow and expensive SWIFT network which relies on multiple intermediary banks.

Enhanced Financial Stability: A CBDC is a direct liability of the sovereign central bank, carrying zero credit or liquidity risk. This is safer than commercial bank deposits, which have a marginal risk of bank failure.

Following the recommendation of the Subhash Chandra Garg Committee (2019) to develop an official digital currency, the RBI launched the e-Rupee pilot project in late 2022.

Current Status

Transaction Volume: Over 150 million transactions recorded, showcasing high retail frequency.

Monetary Value: The ecosystem now manages a value exceeding ₹34,000 crore, indicating trust among high-value corporate users. (Source: Business Standard)

Growth Drivers

Interoperability: A major driver has been the UPI-CBDC interoperability, allowing users to scan any standard UPI QR code to pay using their Digital Rupee wallet.

Offline Functionality: The RBI’s push for offline digital payments has enabled the e₹ to be used in areas with poor internet connectivity, mimicking the "anywhere-anytime" nature of physical cash.

While both are digital, their fundamental nature is different. UPI is a payment interface, whereas the e-Rupee is actual sovereign money.

|

|

e-Rupee (CBDC) |

UPI |

|

Nature of Money |

It is a direct liability of the RBI (Central Bank money). |

It transfers a liability of a Commercial Bank (Commercial Bank money). |

|

Intermediary |

No commercial bank intermediary is required for peer-to-peer settlement. |

Requires a commercial bank to settle the transaction. |

|

Settlement |

Settlement is final and instantaneous, like handing over physical cash. |

Settlement occurs between banks, which can involve a slight delay. |

Bank Disintermediation: If the public moves large sums from commercial bank accounts to safer CBDC wallets, banks could lose a major source of low-cost deposits.

Privacy Concerns: A centralized digital ledger allows the government to track all transactions, raising privacy issues.

Cybersecurity Threats: A centralized national currency ledger is a high-value target for cyberattacks.

The Digital Divide: Effective rollout requires universal access to smartphones, internet, and electricity. This remains a challenge in rural and remote areas of India.

Imposing holding limits on retail CBDC wallets to prevent large-scale deposit flight from commercial banks.

Enacting legislative safeguards to protect user privacy for low-value transactions, potentially through features like "anonymity vouchers" to mimic the privacy of cash.

Positioning the e-Rupee not as a replacement for UPI, but as a resilient sovereign digital backbone that strengthens the financial ecosystem in the new global digital order.

Learn from Global Case Studies

Success- Project mBridge (Geopolitical Impact): A multi-CBDC platform connecting China, UAE, Hong Kong, Thailand, and Saudi Arabia. It shows how CBDCs can create parallel trade settlement systems, reducing dependence on the US dollar.

Struggle - Nigeria’s eNaira (Adoption Issues): Despite being an early adopter, the eNaira faced poor public uptake.

CBDCs are an inevitable evolution of sovereign currency. For India, the e-Rupee offers a path to greater efficiency and strategic autonomy. However, the RBI must proceed with a calibrated and phased approach.

Source: BUSINESS-STANDARD

|

PRACTICE QUESTION Q. With reference to the Digital Rupee (e₹) in India, consider the following statements:

Which of the statements given above are correct? A) 1 and 2 only B) 2 and 3 only C) 1 and 3 only D) 1, 2, and 3 Answer: (C) Explanation: Statement 1 is Correct: The Digital Rupee (e₹) is a Central Bank Digital Currency (CBDC) issued by the Reserve Bank of India (RBI). It is recognized as legal tender, meaning it is a sovereign currency in digital form and is exchangeable one-to-one with physical cash. Statement 2 is Incorrect: The Digital Rupee is not an interest-bearing instrument. Similar to physical cash held in a wallet, holding e₹ in a digital wallet does not generate interest. This design choice distinguishes it from bank deposits and prevents it from destabilizing the banking system by competing directly with savings accounts. Statement 3 is Correct: The RBI has enabled interoperability with the Unified Payments Interface (UPI) QR code infrastructure. This allows users to make payments using the Digital Rupee by scanning standard UPI QR codes at merchant outlets, eliminating the need for merchants to display a separate QR code for e₹. |

A CBDC is a centralized, digital form of a country's sovereign fiat currency, issued and regulated by the central bank, and serves as legal tender. Private cryptocurrencies are decentralized, lack sovereign backing, and their value fluctuates based on speculative market forces.

UPI is merely a payment interface that transfers commercial bank money between accounts. The e-Rupee is central bank money itself. e-Rupee transactions settle instantly on the central bank's ledger without routing through commercial bank backends, eliminating third-party bank failure risks.

Project mBridge is a multi-CBDC platform initiated by the Bank for International Settlements (BIS) connecting central banks like China, the UAE, and Saudi Arabia. It enables direct peer-to-peer international settlements, bypassing slow, expensive traditional rails like SWIFT.

© 2026 iasgyan. All right reserved