Windfall tax is a strategic levy imposed on energy companies earning extraordinary profits due to global price shocks. It aims to generate fiscal revenue, ensure domestic fuel availability, and curb excessive exports while managing inflation and securing India's energy needs.

Why In News?

The Central Government hikes export levies on high-speed diesel to ₹15.50 per litre and Aviation Turbine Fuel (ATF) to ₹14.50 per litre, while reducing the petrol levy to ₹2.50 per litre.

What is Windfall Tax?

Definition: A windfall tax imposes higher rates on specific industries earning unexpected, outsized gains resulting from favorable external conditions rather than internal business innovation.

Origin: India introduces first windfall profit tax in July 2022 to capture super-normal profits during the Russia-Ukraine war, which helped global oil majors double their combined profits to $219 billion in 2022.

Objectives: The government utilizes these extraordinary profits for local needs and redistributive justice, as recommended by the B.K. Chaturvedi Committee (2008).

Importance of Windfall Tax in the Energy Sector

Addressing Price Surges: It targets the "refining spread" when international crude prices exceed reasonable thresholds, specifically capturing gains when Brent crude crosses the $100 per barrel mark.

Stabilizing Domestic Markets: It prevents companies from hoarding or prioritizing exports to bypass local demand, ensuring consistent domestic fuel availability.

Revenue Generation: It provides a vital non-tax revenue stream during economic volatility; when the government slashes excise duties, the fiscal deficit-to-GDP ratio widens by 40-45 basis points, making this tax essential to bridge the gap.

Energy Security: It builds resilience against geopolitical tensions, such as the West Asia crisis and the US-Iran war.

Moderating Exports: The government uses Special Additional Excise Duty (SAED) to discourage excessive export orientation, prioritizing domestic supply over foreign profit margins.

Key Features of the India's Windfall Tax Regime

Applicability: Tax applies as SAED on domestic crude oil production and exports of petrol, diesel, and ATF, though exports to Nepal, Bhutan, Bangladesh, Sri Lanka, Mauritius, and Maldives remain exempt.

Dynamic Tracking: Tax regime links directly to global benchmarks like Brent Crude.

Fortnightly Reviews: The government reviews tax rates every two weeks based on average international crude prices and refining margins.

Temporary Nature: Tax remains dynamic and reduces to zero if global prices crash, ensuring companies avoid penalties during market downturns.

Benefits of Windfall Taxes

Additional Fiscal Revenue: It generates revenue to fund social welfare schemes and fuel subsidies.

Improved Domestic Fuel Availability: It incentivizes oil companies to prioritize the domestic market over seeking higher profit margins abroad.

Reduced Market Distortions During Crises: It captures excess profits to protect the domestic economy from external inflationary shocks and stabilizes inflation.

Better Management of Commodity Price Volatility: It reduces the impact of higher transportation and production costs on domestic consumers.

Protection of Consumer Interests: It shields consumers and domestic Oil Marketing Companies (OMCs) from sharp global crude oil price hikes.

What are the Major Concerns Associated with Windfall Taxes?

Investment Climate: It reduces future investment incentives as investors prioritize the stability of the tax regime.

Policy Uncertainty: Frequent fortnightly revisions disrupt long-term business planning for energy companies.

Export Competitiveness: Additional levies reduce the global competitiveness of export-oriented firms.

Defining "Windfall": Distinguishing between actual windfall profits and normal business gains remains complex.

Bond Market Impact: Concerns over fiscal revenue loss versus inflation relief cause 10-year G-Sec yields to jump 5-8 bps on announcement days.

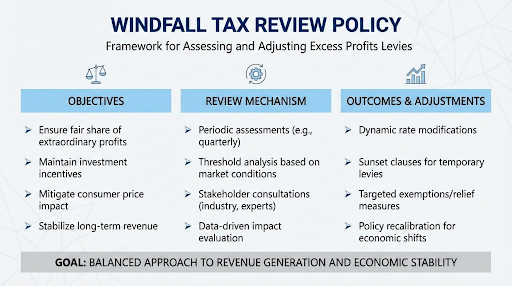

What Measures Can Improve the Effectiveness of Windfall Taxes?

Transparent Taxation Criteria: Define clear, well-defined criteria for the application of windfall taxes to avoid arbitrary levies.

Predictable Review Mechanisms: Governments should avoid retrospective application and maintain a predictable, formula-based fortnightly review system.

Balancing Industry Incentives and Public Interest: Windfall taxes should remain sector-specific, rather than company-specific, to maintain market fairness.

Strengthening Domestic Energy Infrastructure: Policies must encourage higher domestic production of crude oil to structurally mitigate the impact of global price shocks.

Diversifying Energy Sources: The country needs to accelerate its Bio-Economy to reduce reliance on fossil fuels and limit exposure to crude oil volatility.

Enhancing Strategic Petroleum Reserves: India must develop salt-cavern based strategic oil reserves to act as a buffer stock against supply disruptions and price shocks.

Windfall taxes function as a fiscal stabilizer, ensuring that extraordinary corporate profits generated by global price shocks are redistributed to maintain domestic energy security and macroeconomic stability.

Source: NEWINDIANEXPRESS

|

PRACTICE QUESTION Q. Consider the following statements regarding 'Windfall Tax' in India: 1. It is permanently levied on companies to capture their operational profits. 2. In India, it is levied as a Special Additional Excise Duty (SAED) on petroleum exports. 3. Public sector oil companies exporting to Nepal and Bhutan are exempt from this export duty. Which of the statements given above is/are correct? A) 1 and 2 only B) 2 and 3 only C) 1 and 3 only D) 1, 2, and 3 Answer: B Explanation: Statement 1 is incorrect: The Windfall Tax is not permanently levied. It is a temporary measure introduced in July 2022 to tax the "super-normal" profits of oil companies resulting from volatile global crude prices. The tax rates are reviewed fortnightly (every two weeks) by the government based on average oil prices in the preceding two weeks and are adjusted (raised, lowered, or scrapped) accordingly. Statement 2 is correct: In India, the windfall tax on the export of petroleum products (specifically petrol, diesel, and aviation turbine fuel/ATF) is levied in the form of a Special Additional Excise Duty (SAED). While a windfall tax is also levied on domestically produced crude oil (as a cess per tonne), the export component is specifically structured as SAED. Statement 3 is correct: Exports of petroleum products (like petrol and diesel) to neighboring countries such as Nepal and Bhutan are exempt from this Special Additional Excise Duty (SAED). These countries rely on India for their fuel supplies, which are typically fulfilled by public sector oil marketing companies (like IOCL) under bilateral treaties, and thus are not subject to the export duties intended for the broader international market. |

© 2026 iasgyan. All right reserved