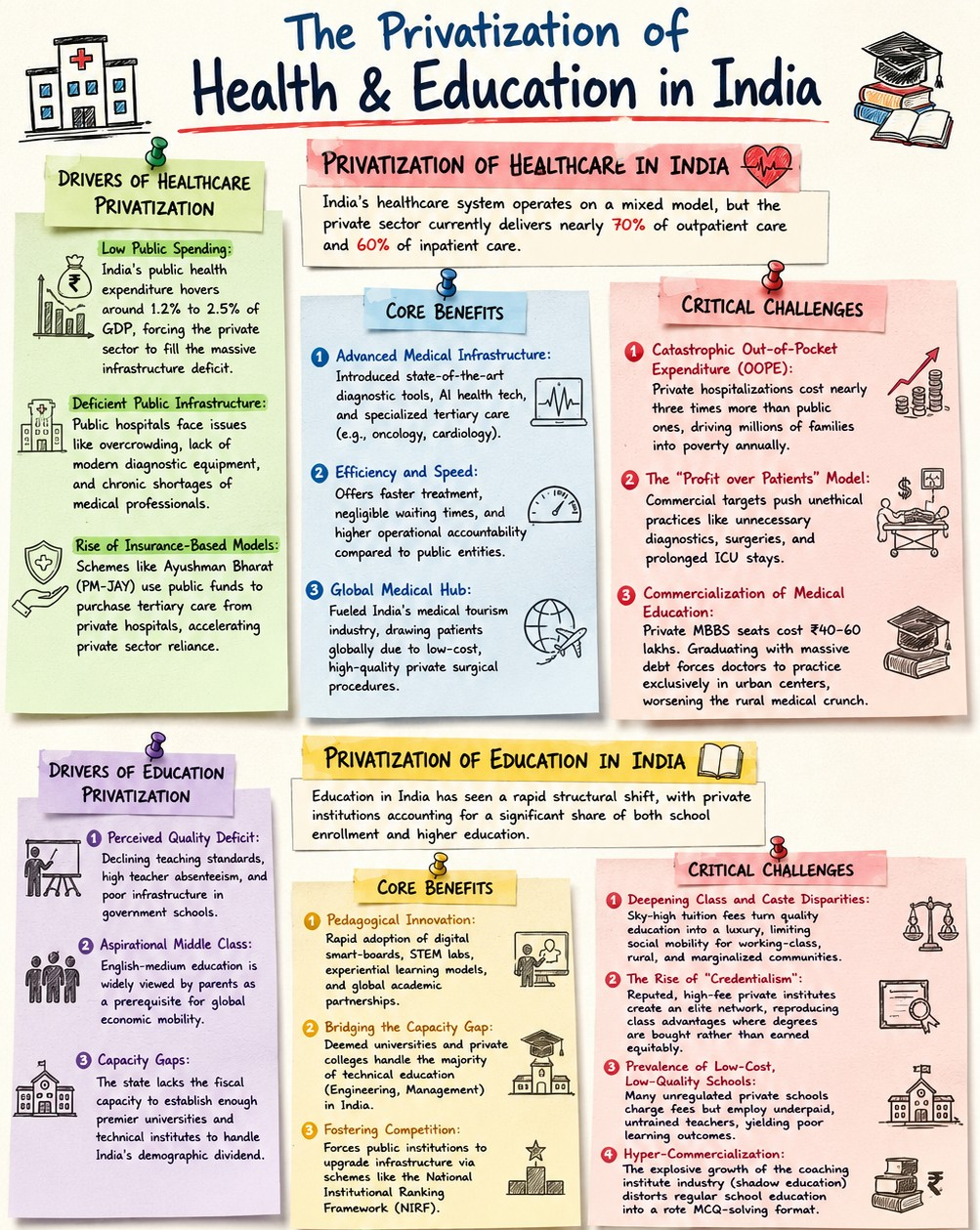

India’s social infrastructure faces rapid consolidation as foreign private equity and venture capital funds inject US$ 36 billion in 2025, acquiring controlling stakes in over 70% of leading private hospital chains.

Rising Demand for Quality Services

Demographic Dividend: India possesses the world’s largest youth population, featuring 580 million individuals aged 5-24, which creates an unprecedented demand for K-12 and higher education. (Source: IBEF 2026)

Epidemiological Transition: A rapidly aging population and a surging burden of Non-Communicable Diseases (NCDs) drive consistent, long-term utilization of tertiary and specialized healthcare services.

Public Sector Capacity Constraints

Underfunded State Infrastructure: The Union Budget 2026-27 exposes a declining priority for health, with public spending falling to a mere 0.28% of GDP.

Educational Investment Shortfalls: Government expenditure on education stood at 4.12% of GDP in FY2022, well below the required threshold to modernize the massive public school network.

Attractive Long-Term Investment Opportunities

Favorable FDI Policies: The government permits 100% Foreign Direct Investment (FDI) through the automatic route for both greenfield and brownfield hospital acquisitions, removing regulatory hurdles for global funds.

Predictable Unit Economics: Investors target single-specialty chains (oncology, IVF, ophthalmology) due to their scalable models, regularly securing high-teens EV/EBITDA (earnings before interest, tax, depreciation and amortisation) returns.

Technological Transformation

EdTech and AI Booms: Integration of Artificial Intelligence and digital learning triggers a fivefold funding surge in EdTech platforms in H1 2025. (Source: Bain & Company)

Digital Health Infrastructure: Innovations in telemedicine and AI-powered Clinical Decision Support Systems (CDSS) draw immense venture capital to modernize diagnostic and remote care platforms.

What are the Positive Implications of Growing Private Participation?

What are the Positive Implications of Growing Private Participation?Expansion of Infrastructure

Bridging Capacity Deficits: Private equity (PE) funding constructs massive capacity; for example, the Blackstone-backed CARE Hospitals initiates debt-enabled expansions to add 3,500 beds by FY27. (Source: CRISIL)

Improved Quality and Efficiency

Operational Excellence: Private capital introduces standardized clinical protocols and streamlines back-office administration, reducing operational waste and bringing economies of scale to fragmented medical practices.

Greater Innovation and Research

Cutting-Edge R&D: Private equity funds inject vital capital into life sciences, backing over 1,800 global companies to advanced medical devices and mRNA vaccine developments.

Employment Generation

Skilled Workforce Demand: Rapid expansion of private health and education hubs requires massive hiring, catalyzing the creation of specialized jobs for allied healthcare professionals, teachers, and technical staff.

Reduced Fiscal Burden on Government

Supplementing State Welfare: Private investments shoulder heavy capital expenditure burdens, allowing the state to leverage private infrastructure for public schemes, such as empanelling private hospitals under Ayushman Bharat (PMJAY).

Commercialisation of Essential Services

Profit Over Patients: Corporate hospitals prioritize financial metrics, specifically Average Revenue Per Occupied Bed (ARPOB) and EBITDA margins, sidelining low-cost, essential preventive care.

Rising Costs and Affordability Concerns

Explosive Medical Inflation: The ARPOB in PE-backed hospital chains skyrocketed by 42% between 2019 and 2024, decisively outpacing baseline medical inflation and burdening patients (Source: CRISIL, 2024).

Growing Inequality

Exclusionary Access: The proliferation of high-fee private schools and premium healthcare chains creates a sharp divide, excluding vulnerable populations and turning fundamental rights into luxury commodities.

Risk of Excessive Financialisation

Wealth Extraction Models: Investors deploy the OpCo-PropCo (Operating Company/Property Company) model, separating real estate from hospital operations. They sell land to Real Estate Investment Trusts (REITs) to pay out massive dividends, saddling healthcare providers with unsustainable long-term rents.

Regulatory and Ethical Challenges

Physician Moral Injury: Profit-driven quotas force doctors into ethical compromises; 44% of physicians report an inability to deliver medically necessary treatments due to stringent insurance barriers. (Source: National Health Program)

Consolidation of Hospital Chains

Monopolistic Mergers: PE firms execute aggressive "buy-and-build" strategies, merging regional healthcare providers into massive national platforms, which stifles local market competition.

Better Technology Adoption

Advanced Clinical Tools: Corporate hospitals deploy vast capital to import state-of-the-art diagnostic equipment and adopt AI-driven telemedicine, enhancing complex surgical and treatment outcomes.

Concerns About Patient Affordability

The Morbidity Paradox: Access expands, but financial ruin follows. The average cost for a private hospital admission stands at ₹50,508, which is nearly eight times higher than a public hospital admission at ₹6,631. (Source: NSS 80th Round)

Professionalisation of School Management

Data-Driven Governance: Corporate-backed schools implement sophisticated data analytics, continuous teacher training, and professional governance models to drastically improve school administration.

Expansion of Private Educational Networks

Dominating the K-12 Sector: The private sector steps in where state capacity fails, currently teaching over 120 million students across India (Source: Independent Think Tank Estimates).

Risk of Educational Exclusion

The "Coaching Factory" Epidemic: Deep commercialization transforms students into "customers", fostering environments that prioritize rote memorization and competitive exam results over socio-emotional wellbeing and holistic pedagogy.

Strengthening Regulatory Oversight

Independent Authorities: Establish a statutory Healthcare Investment Regulatory Authority to monitor aggressive financial leverage, enforce debt caps (e.g., maximum 2.5x EBITDA), and review anti-competitive "OpCo-PropCo" maneuvers,.

Expanding Public Investment in Health and Education

Meeting Fiscal Targets: The government must scale sovereign funding to meet the 2.5% (Health) and 6% (Education) GDP targets, thereby upgrading public infrastructure to compete with the private sector.

Promoting Public-Private Partnerships (PPPs)

Strategic Contracting: Embed "Golden Shares" within PPP concession agreements. This grants the State non-economic veto power to block predatory ownership changes or value extraction that threatens the public good.

Ensuring Affordability Through Targeted Subsidies

Performance-Linked Funding: Tie government Viability Gap Funding (VGF) and annuity payments directly to a composite index measuring affordability, clinical quality, and sustained capital reinvestment.

Enhancing Transparency and Accountability

Mandatory Disclosures: Require all private hospitals to publicly publish mortality rates, surgical outcomes, and standardized procedural costs on a central portal to eliminate information asymmetry and enforce market discipline.

Protecting Equity and Universal Access

Hard-Wiring Free Care Quotas: Enforce stringent FDI approval conditions that explicitly mandate private operators to reserve 25% of beds for EWS/BPL patients at highly subsidized (CGHS) rates.

India must wield "idealism without illusions," harnessing private capital's efficiency while enforcing regulations to ensure health and education remain universally accessible constitutional rights rather than exclusionary market commodities.

Source: INDIANEXPRESS

|

PRACTICE QUESTION Q. "The growing role of private capital in healthcare and education presents both opportunities and challenges for India's human development trajectory." Critically Analyze. (250 Words, 15 Marks). |

Firms are drawn by India's massive demographic dividend (580 million youth) and high disease burden. The allowance of 100% FDI via the automatic route enables investors to consolidate fragmented assets, apply "buy-and-build" models, and extract high-teens EV/EBITDA multiples.

Private capital introduces advanced medical technologies (like robotics and mRNA vaccines), standardizes clinical and school management protocols, eliminates administrative waste, and rapidly builds missing tertiary care and K-12 infrastructure.

The primary risk is the "morbidity paradox," where capacity exists but becomes too expensive, driving high out-of-pocket expenditure (44%). Aggressive models like OpCo-PropCo extract capital as dividends rather than reinvesting in patient care, leading to severe inequality in access.

Governments must establish independent regulatory bodies to curb price gouging, redesign PPP contracts with strict financial-conduct covenants, implement a "Golden Share" to veto predatory takeovers, and massively boost sovereign spending to 2.5% of GDP for health and 6% for education.

© 2026 iasgyan. All right reserved