The right to collect toll on existing highways would be offered for 30 years or so to private investors in return for an upfront payment.

Oil and gas pipelines would similarly be leased to private players as would seaports and airports.

Assets proposed for monetisation include airports, terminals in seaports, railway lines, railway stations, stadiums, warehouses and a host of other government assets with unutilised potential.

Criticisms:

leasing was not the best option because outright sale would bring in greater value and avoid the ticklish questions of asset stripping and maintenance of the leased assets.

leased assets would not be properly maintained. After all, no one washes a hired car.

whether monetisation is intended to substitute the skill and efficiency of the private sector for the supposed lethargy of government control.

the move would bring greater concentration of power in the hands of the private sector are not relevant.

when the private sector bids for these projects, they would probably require institutional finance for at least part of their outlay and this would result in a “crowding out” of other investments.

Way Around:

the agreement to lease could contain clauses that mandate the return of assets in the same condition in which they were offered, normal wear and tear excepted.

If leasing out a government asset brings improved efficiency in management that would be an additional bonus.

Every time the government cedes some ground by opening sectors hitherto reserved exclusively for itself, it runs this risk. This has not prevented them from allowing private operators to operate freight trains or terminals in seaports.

Public sector undertakings (PSUs) raise funds from banks and even the National Highways Authority of India (NHAI) resorts to public funding. We do not ban PSUs or the NHAI from raising funds in the market.

Necessary checks can easily be built into the offer documents that will ensure that the scheme does not create or reinforce monopolies of any sort.

About the Programme:

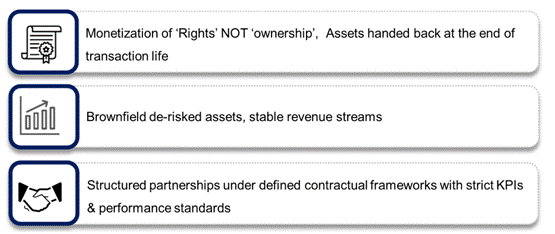

At its core, the idea is to lease out brownfield projects, proceeds from which can be used to finance greenfield projects.

The ownership of the assets monetised, though, will remain with the government, with the private players taking on the operational risk.

While roads, railways and power account for around 65 per cent of the proceeds of the programme, the list of assets detailed is spread across sectors such as telecom, aviation, mining and warehousing, suggesting a more wide-ranging programme.

Benefit of the Programme:

Asset monetization, based on the philosophy of Creation through Monetisation, is aimed at tapping private sector investment for new infrastructure creation.

This is necessary for creating employment opportunities, thereby enabling high economic growth and seamlessly integrating the rural and semi-urban areas for overall public welfare.

The strategic objective of the programme is to unlock the value of investments in brownfield public sector assets by tapping institutional and long-term patient capital, which can thereafter be leveraged for further public investments.

NMP is envisaged to serve as a medium-term roadmap for identifying potential monetisation- ready projects, across various infrastructure sectors.

The NMP is aimed at creating a systematic and transparent mechanism for public authorities to monitor the performance of the initiative and for investors to plan their future activities.

Asset Monetisation needs to be viewed not just as a funding mechanism, but as an overall paradigm shift in infrastructure operations, augmentation and maintenance considering private sector’s resource efficiencies and its ability to dynamically adapt to the evolving global and economic reality.

New models like Infrastructure Investment Trusts & Real Estate Investment Trusts will enable not just financial and strategic investors but also common people to participate in this asset class thereby opening new avenues for investment.

Framework of Asset Monetisation Programme:

Monetization through disinvestment and monetization of non-core assets have not been included in the NMP. Further, currently, only assets of central government line ministries and CPSEs in infrastructure sectors have been included.

Process of coordination and collation of asset pipeline from states is currently ongoing and the same is envisaged to be included in due course.

This includes selection of de-risked and brownfield assets with stable revenue generation profile with the overall transaction structured around revenue rights.

Estimated Potential:

The period for NMP has been decided so as to be co-terminus with balance period under National Infrastructure Pipeline (NIP).

The aggregate asset pipeline under NMP over the four-year period, FY 2022-2025, is indicatively valued at Rs 6.0 lakh crore.

The estimated value corresponds to ~14% of the proposed outlay for Centre under NIP (Rs 43 lakh crore).

The sectors included are roads, ports, airports, railways, warehousing, gas & product pipeline, power generation and transmission, mining, telecom, stadium, hospitality and housing.

In terms of annual phasing by value, 15% of assets with an indicative value of Rs 0.88 lakh crore are envisaged to be rolled out in the current financial year (FY 2021-22).