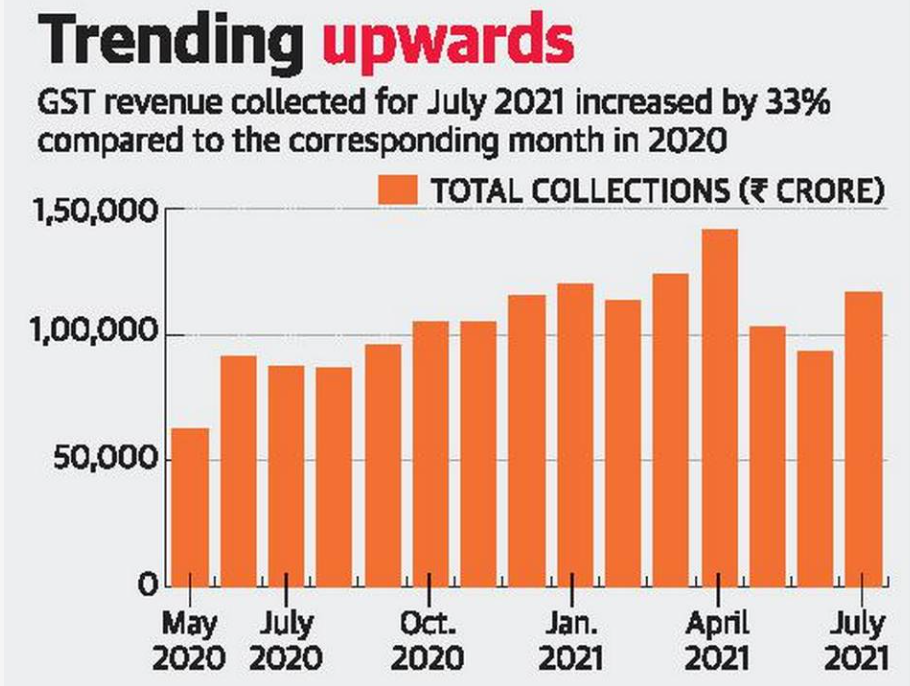

The gross Goods and Services Tax (GST) revenues in July recovered sharply to Rs. 1,16,393 crore.

Goods and Services Tax

GST, or Goods and Services Tax, is an indirect tax that customers have to bear when they buy any goods or services, such as food, clothes, electronics, items of daily needs, transportation, travel, etc.

It is levied on the manufacturer or seller goods and the providers of services.

The sellers usually add the tax expense into their costs, and the price the customers pay is inclusive of GST.

Benefits of GST in India

GST was brought in as a revolutionary change and India‘s biggest tax system overhaul since Independence. GST replaced a plethora of indirect taxes such as states‘ sales tax, service tax, excise, etc., with a single central tax regime applied uniformly on all products and services.

However, the biggest benefit of GST was that it opened up entire India as a single unified market allowing for free movement of goods across states‘ borders, as opposed to the earlier scenario where state borders became barriers.

GST allowed for faster movement of trucks and led to requirements for fewer warehouses across several states.

However, GST has multiple tax rate slabs for different categories of products – a fact that still makes it more complicated than many expected.

What are the different types of GST?

Central GST (CGST): GST paid on each transaction is divided into two equal parts: the part for the Centre is termed as CGST.

State GST (SGST): The part of a state‘s share of GST, when a transaction takes place within the state, is called SGST.

Union territory GST (UGST): When a transaction takes place within a union territory (UT) without a legislature, the part of GST that the UT gets is called UGST.

Integrated GST (IGST): When a transaction takes place between two states/UTs or between a state/UT and any foreign territory, IGST is levied without any bifurcation on the applicable GST rate.

What items are not taxed or covered under GST?

There are a few products, which were not under the purview of GST till long after its launch.

Alcohol for human consumption: On alcohol, the power to tax remains with the states.

Petroleum products: GST was not imposed on five petroleum products — crude oil, diesel, petrol, natural gas and ATF.

Tobacco: Along with GST, the Central Government has the power to levy additional excise duty on tobacco products.

Entertainment tax: The power to decide on entertainment tax levied by local bodies remains with the states.

Also, there are some exceptions on Indian Railways tickets, where instead of the destination, the origin of the journey is taken into consideration. For example, if Rajdhani Express is registered in Delhi, on the tickets from Delhi, CGST an SGST will be levied, while IGST will be charged when the journey originates at a place other than Delhi.

GST Council

The GST council is the key decision-making body that takse all important decisions regarding the GST.

The GST Council dictates tax rate, tax exemption, the due date of forms, tax laws, and tax deadlines, keeping in mind special rates and provisions for some states.

The predominant responsibility of the GST Council is to ensure to have one uniform tax rate for goods and services across the nation.

Structure of GST Council

GST Council is a joint forum for the Centre and the States. It consists of the following members:

The Union Finance Minister is the Chairperson

As a member, the Union Minister of State is the in charge of Revenue of Finance

The Minister in charge of finance or taxation or any other Minister nominated by each State government, as members.

GST Council recommendations

Article 279A (4) specifies that the Council can make recommendations to the Union and the States on the important issues related to GST, such as, the goods and services will be subject or exempted from the Goods and Services Tax.