Celebrating 11 years, the PMMY has revolutionized grassroots credit by disbursing ₹40 lakh crore to the "unfunded." To sustain India’s $5 trillion vision, it must now leverage AI-driven risk appraisal and cash-flow-based lending to address rising NPAs and information asymmetry.

Why In News?

The Pradhan Mantri MUDRA Yojana (PMMY) completes 11 years of providing collateral-free loans to small and micro-entrepreneurs to promote self-employment and financial inclusion.

What is Pradhan Mantri Mudra Yojana (PMMY)?

It was launched on April 8, 2015, to facilitate collateral-free institutional credit to non-corporate, non-farm small and micro-enterprises.

It operates under the Department of Financial Services (DFS), which is part of the Ministry of Finance.

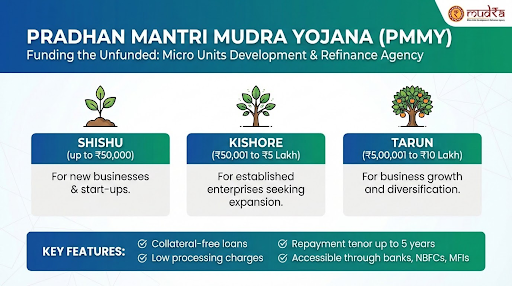

Core Purpose: Provides loans up to ₹20 Lakh to income-generating micro-enterprises engaged in manufacturing, trading, and services sectors, including activities allied to agriculture like poultry and dairy.

Lending Institutions: Loans are extended by Member Lending Institutions (MLIs) such as Scheduled Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks, MFIs, and NBFCs.

Objectives

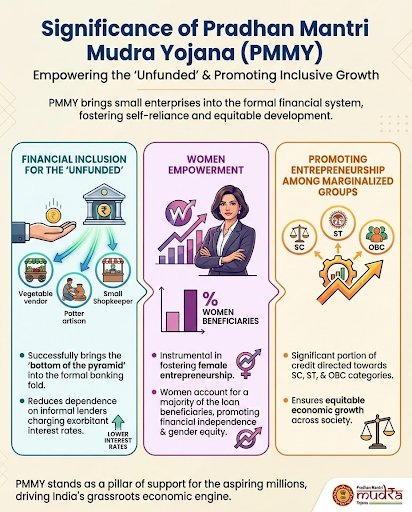

Financial Inclusion: Providing collateral-free formal credit to "bottom of the pyramid" entrepreneurs.

Employment Generation: Facilitating job creation by supporting self-employment with capital.

Formalizing the Informal Sector: Mainstreaming non-corporate small businesses to expand the tax base and financial access.

Lender Regulation: Monitoring interest rates and protecting clients through MFI registration and financing.

Key Features of Pradhan Mantri Mudra Yojana (PMMY)

Loan Categories: The scheme offers four categories of loans based on the stage of business growth

Collateral-Free Credit: Borrowers are not required to provide any collateral or security to avail of these loans.

Mudra Card: Borrowers receive a RuPay debit card for easy working capital access, enabling withdrawals and point-of-sale transactions.

Credit Guarantee: PMMY loans are backed by the Credit Guarantee Fund for Micro Units (CGFMU), protecting lenders from defaults.

Achievements of Pradhan Mantri Mudra Yojana

Total Sanctions: The scheme has sanctioned over 57.7 crore loans with a cumulative amount of approximately ₹40.07 Lakh Crore since its inception. (Source: PIB)

Women Beneficiaries: Women borrowers accounted for 59.81% of the total number of loan accounts, with a total share of 37.45% in disbursed amounts. (Source: PIB)

Social Inclusion: The cumulative share of SC, ST, and OBC categories stood at 45.52% in terms of loan accounts and 31.77% in terms of the total disbursed amount. (Source: PIB)

New Entrepreneurs: New entrepreneurs constituted 21% of total loan accounts and accounted for a 30.09% share of the total disbursed amount. (Source: PIB)

Low NPA Levels: The Non-Performing Assets (NPAs) under the scheme have witnessed a decline, dropping to 2.1% in FY24, indicating improved credit discipline.

What are the Challenges faced by Pradhan Mantri Mudra Yojana (PMMY)?

Asset Quality: Despite fluctuating NPA levels, higher defaults exist in the Shishu category due to high monitoring costs for small loans. (Source: RBI)

Financial Literacy Gaps: Poor digital and documentation skills among micro-entrepreneurs often lead to fund mismanagement.

Monitoring Difficulties: The high volume of small loans complicates tracking, increasing the risk of fund diversion.

Regional Disparity: Disbursements favor developed states, leaving rural areas underserved by banking infrastructure.

Credit History: A lack of formal history for first-time borrowers hinders accurate creditworthiness assessments.

Way Forward

Tech-Driven Monitoring: Utilizing AI and Machine Learning for credit scoring and early warning systems can preemptively identify defaults.

Post-Credit Support: Transitioning to "credit plus" services by offering market linkages, branding, and financial literacy training.

Digital Adoption: Promoting the Mudra Card and digital payments creates a footprint for easier future credit assessments.

Specialized Products: Customizing loans for specific sectors to align with unique cash-flow cycles.

Conclusion

PMMY has revolutionized micro-finance by aiding the "unfunded." With 57 crore beneficiaries, it boosts entrepreneurship and women's empowerment. Addressing regional and quality gaps through data-driven support will ensure it remains key to India's inclusive $5 trillion economy goal

Source: ANINEWS

|

PRACTICE QUESTION Q. Consider the following statements regarding the Pradhan Mantri MUDRA Yojana (PMMY): 1. MUDRA Ltd. operates as a direct lending institution to micro-enterprises. 2. The 'Tarun Plus' category provides collateral-free loans up to ₹20 lakh for successful micro-firms. 3. The Credit Guarantee Fund for Micro Units (CGFMU) covers the lender's risk under the scheme. Which of the statements given above are correct? a) 1 and 2 only b) 2 and 3 only c) 1 and 3 only d) 1, 2, and 3 Answer: b Explanation: Statement 1 is incorrect. MUDRA (Micro Units Development & Refinance Agency) Ltd. does not lend directly to micro-entrepreneurs or individuals. It functions as a refinancing agency. It provides financial support to intermediaries such as Commercial Banks, RRBs, Small Finance Banks, MFIs, and NBFCs, which in turn lend directly to the borrowers. Statement 2 is correct. A new category called 'Tarun Plus' was introduced (announced in the Union Budget 2024-25) to provide loans ranging from ₹10 lakh to ₹20 lakh. This category is specifically for entrepreneurs who have previously availed and successfully repaid loans under the 'Tarun' category. Like other PMMY loans, these are collateral-free. Statement 3 is correct. To mitigate the issue of collateral for these micro-loans, the Credit Guarantee Fund for Micro Units (CGFMU) was created. It provides a guarantee to the lending institutions (Member Lending Institutions) against default, covering a significant portion of the risk (75%). |

Launched in 2015, PMMY is a flagship Indian government scheme that provides collateral-free microcredit to non-corporate, non-farm small and micro-enterprises to promote financial inclusion, local employment, and grassroots entrepreneurship.

MUDRA loans are divided into lifecycle-based stages tailored to business growth: Shishu (up to ₹50,000 for early stages), Kishor (₹50,001 to ₹5 lakh for operational stabilization), Tarun (₹5,00,001 to ₹10 lakh for scale-ups), and the newly added Tarun Plus (up to ₹20 lakh).

Introduced in the Union Budget 2024-25, the Tarun Plus category provides collateral-free loans up to ₹20 lakh exclusively for entrepreneurs who have demonstrated a stable repayment track record under previous Tarun loans, assisting them in scaling to medium-sized enterprises.

© 2026 iasgyan. All right reserved