India’s digital lending boom, powered by JAM and AI, aids MSME credit access but raises concerns over predatory apps and data misuse. Measures like RBI’s app directory, MeitY actions, and SRO-FT aim to balance innovation with consumer protection and regulation.

Copyright infringement not intended

Picture Courtesy: newsage

Context

The Reserve Bank of India (RBI) and the Government of India are strengthening the regulatory framework for the digital lending ecosystem.

What is Digital Lending?

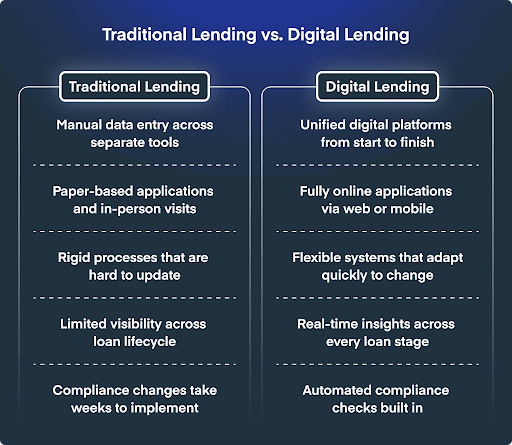

Digital lending is a remote and automated process that uses digital technologies—such as mobile apps and web platforms—for the entire loan lifecycle, including customer acquisition, credit assessment, loan approval, disbursement, and recovery.

In India, it is regulated by the Reserve Bank of India (RBI) to ensure transparency and borrower protection.

How Digital Lending Works?

Application & Verification: Borrowers apply via mobile apps or websites, uploading digital documents like ID proof and bank statements.

Credit Assessment: Platforms use advanced algorithms and artificial intelligence (AI) to evaluate creditworthiness; looking at alternative data like utility bill payments or transaction history.

Instant Disbursal: Once approved, funds are transferred directly into the borrower's bank account.

Direct Repayment: Loan repayments are managed online, through automated direct debits or the platform's payment gateway.

Why is India's Digital Lending Sector Booming?

Bridging the Credit Gap

Digital lenders are filling credit void for Micro, Small, and Medium Enterprises (MSMEs). About 87% of India's 63.3 million MSMEs lack access to formal credit, creating a shortfall of ₹20–25 trillion (Source: Nexdigm).

Leveraging Digital Public Infrastructure (DPI)

The success of the JAM Trinity (Jan Dhan, Aadhaar, Mobile) and the Unified Payments Interface (UPI) provides a robust foundation for instant, paperless loan disbursal.

Alternative Credit Scoring

Fintech lenders use Artificial Intelligence (AI) and Machine Learning (ML) to analyze alternative data (like digital transaction history) for rapid loan underwriting, unlike traditional banks that rely on collateral and formal credit scores.

What are the Challenges With Digital Lending?

Predatory Lending and Usurious Interest Rates

Unregulated apps often exploit borrowers through exorbitant hidden charges and high compound interest rates disguised as fees. This leads to debt traps for vulnerable individuals.

Data Privacy and Security Violations

Illegal loan apps often force users to grant access to their phone contacts, photo galleries, and location data. A direct violation of the Right to Privacy, which was declared a fundamental right under Article 21 in the K.S. Puttaswamy v. Union of India (2017) judgment.

Regulatory Arbitrage and Money Laundering

Many malicious apps operate through shell companies and offshore entities to evade Indian laws. This structure facilitates money laundering and poses a threat to the nation's financial stability.

Government and RBI's Regulatory Framework

|

Regulatory Body / Initiative |

Key Actions and Mandates |

|

Reserve Bank of India (RBI) |

|

|

MeitY & Ministry of Home Affairs (MHA) |

|

|

Grievance Redressal Mechanisms |

The 'SACHET' portal allows citizens to lodge complaints against illegal money collection, monitored by the State Level Coordination Committee (SLCC). |

|

State Governments (Cooperative Federalism) |

Since 'Police' and 'Public Order' are State subjects under the Seventh Schedule, State Law Enforcement Agencies are the primary bodies for investigating and prosecuting these illegal apps. |

Way Forward

Empowering Self-Regulation

The RBI must accelerate the formation of a Self-Regulatory Organisation for the FinTech Sector (SRO-FT) to enforce a code of conduct and baseline technology standards.

Strengthening Legal Action

The government should ban the Unregulated Lending Activities and ensure stricter criminal prosecution of illegal app operators, moving beyond just blocking apps.

Capacity Building

State law enforcement agencies must be upgraded with skills and technology to effectively investigate complex, cross-border cyber-financial crimes.

Learn Lessons from Global Best Practices

|

Country |

Key Initiative |

Learning for India |

|

United Kingdom |

The Financial Conduct Authority's (FCA) 'Consumer Duty' framework (2023) legally requires lenders to prove their products offer fair value and do not cause foreseeable harm. |

India can adopt a similar 'prove-no-harm' mandate to enhance consumer protection. |

|

Singapore |

The Monetary Authority of Singapore (MAS) uses an efficient regulatory sandbox to test new fintech apps in a controlled environment before public launch. |

A similar sandbox model can help stress-test data security and algorithmic fairness of new apps in India. |

Conclusion

Balancing innovation with robust regulation is key to ensuring that digital lending becomes a tool for financial empowerment, not exploitation.

Source: PIB

|

PRACTICE QUESTION Q. The 'SACHET' portal, often seen in the news, is associated with which of the following? a) Registering MSMEs for institutional credit. b) Lodging complaints against illegal money collection entities. c) A unified platform for fast-tracking environmental clearances. d) Regulating cryptocurrency transactions in India. Answer: b Explanation: The SACHET portal allows citizens to lodge complaints against unauthorized money collection and illegal lending entities. It is monitored by the inter-regulatory State Level Coordination Committee (SLCC). |

Digital lending involves extending credit through digital platforms, leveraging technology for faster processing, instant disbursal, and alternative credit scoring, primarily targeting underserved segments like MSMEs.

Key challenges include predatory lending with exorbitant hidden charges, unauthorized access to user data violating privacy rights, severe harassment by recovery agents, and regulatory arbitrage leading to potential money laundering.

The RBI mandates that loan disbursals and repayments occur directly between the borrower and the Regulated Entity (RE). Furthermore, RBI has mandated a public directory of Digital Lending Apps (DLAs) via the CIMS portal, effective July 2025.

© 2026 iasgyan. All right reserved