Description

Disclaimer: Copyright infringement not intended.

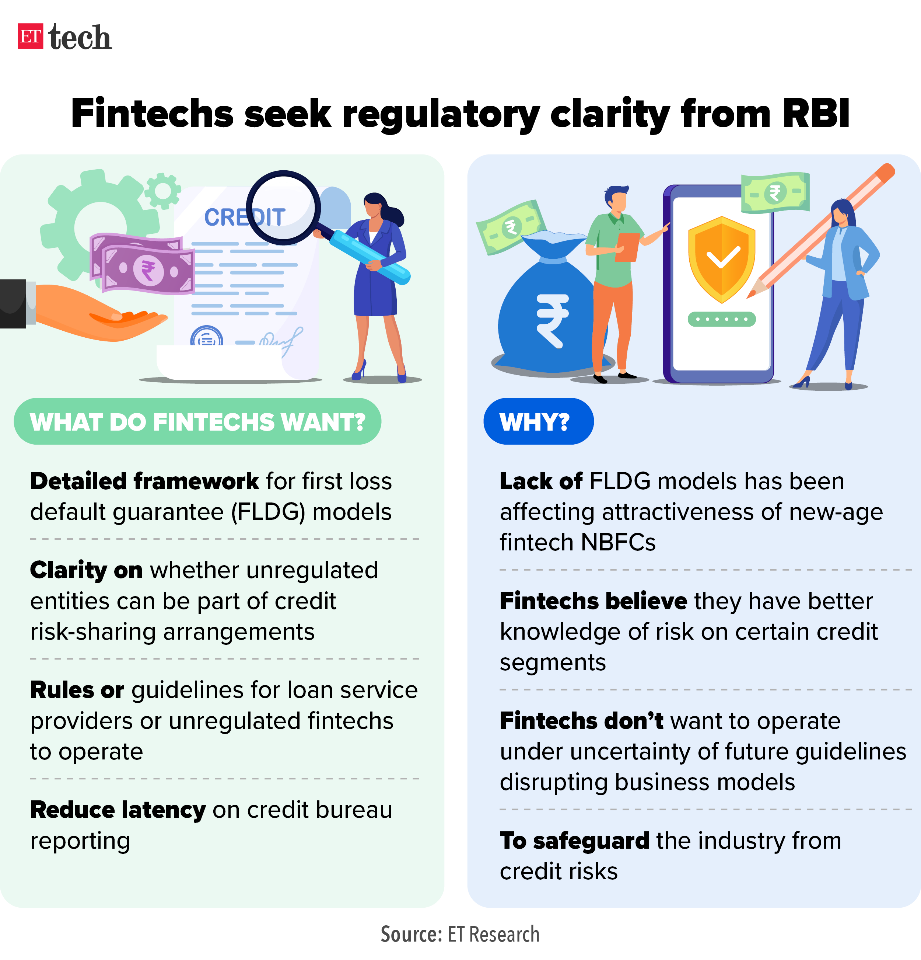

Context

- Fintech lenders are exploring alternative business models after the first loss default guarantee (FLDG) arrangement was barred by the Reserve Bank of India (RBI) under the digital lending norms.

What is FLDG?

- FLDG or ‘First Loan Default Guarantee’ is an arrangement between a fintech company and regulated entity (RE), including banks and non-banking finance companies, wherein the fintech compensates the RE to a certain extent if the borrower defaults.

- The bank/NBFC partners lend through the fintech but from their own books. FLDG helps expand the customer base of traditional lenders but relies on the fintech's underwriting capabilities.

.jpeg)

Lack of clarity (Previously)

- According to fintech firms, the RBI has been vague about FLDG and there is no clarity on what is permissible and what is not permissible as far as these partnerships are concerned.

- Banks, NBFCs, and Fintechs have sought clarification from the RBI on First Loss Default Guarantee (FLDG), on which RBI has advised the regulated entities to follow its directions on securitisation, especially, synthetic securitisation.

- Synthetic securitization means a structure where the credit risk of an underlying pool of exposures is transferred through the use of credit derivatives or credit guarantees to hedge the credit risk of the portfolio. This is an issue on which RBI needed to give more clarity as the guidelines just refer to the earlier issued securitisation norms.

Read: https://www.iasgyan.in/daily-current-affairs/rbis-guidelines-on-digital-lending-and-first-loss-digital-guarantee

Current Scenario

- Currently, the industry is examining co-lending arrangements and alternative models which can balance the right incentives in the partnership for performance and risk sharing.

- Currently, digital lenders are at initial stages of developing business models, with lenders depending on the repayment proficiency of the portfolio.

Collection Efficiency Model

- Fintechs are looking at a collection efficiency model which stipulates that banks and non-banking finance companies (NBFC) will pay a fee to them in proportion to the collection track record of the portfolio.

- Fintechs can become a collection agency for the lender and earn a fee that would be deducted from their payout if they do not achieve the target.

Revenue-Sharing Model

- Another option is a revenue-sharing model where lenders will share the interest income with them, depending on delinquencies of borrowers.

- Under this arrangement, if defaults rise, the share of the lender will go up and that of the fintech will go down.

- Besides exploring new structures, many fintech lenders are moving towards co-lending agreements with regulated entities to avoid any compliance risk.

Closing Remarks

- Despite considering alternative models, Fintechs players are cautious before adopting them.

- One reason is that they are expecting the RBI to soon come out with the clarification on FLDG.

- Another reason is that Fintechs do not want to rush into new business models and then get caught in the tangle of regulatory compliance.

The trust between the fintech and bank for such arrangements will come only when the relationship becomes seasoned.

https://indianexpress.com/article/business/banking-and-finance/banks-nbfcs-stop-lending-to-apps-under-loan-default-guarantee-model-8456993/