Disclaimer: Copyright infringement not intended.

Context:

What are AT1 bonds?

.jpeg)

Purpose of AT1 Bonds:

|

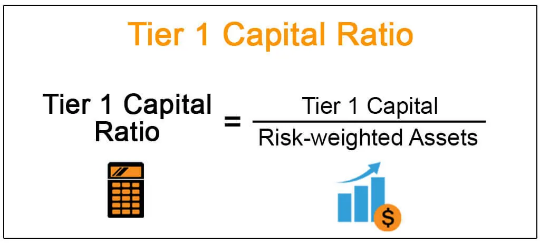

Tier 1 Capital vs. Tier 2 Capital: An Overview A bank's capital consists of tier 1 capital and tier 2 capital,

A bank's total capital is calculated by adding its tier 1 and tier 2 capital together. Components of Tier 1 Capital Tier 1 Capital = Common Equity Tier 1 Capital + Additional Tier 1 Capital 1. Common Equity Tier 1 (CET1) Capital – CET1 capital is the core equity capital of the bank and includes shareholders equity, retained earnings, and accumulated other comprehensive income of the bank. 2. Additional Tier 1 (AT1) Capital – AT1 capital includes certain contingently convertible and perpetual debt of the bank since they provide going concern capital to the bank. Under Basel III, the minimum tier 1 capital ratio is 10.5%, which is calculated by dividing the bank's tier 1 capital by its total risk-weighted assets (RWA). In India, one of the key new rules brought in was that banks must maintain capital at a minimum ratio of 11.5 percent of their risk-weighted loans. Of this, 9.5 percent needs to be in Tier-1 capital and 2 percent in Tier-2. Tier-1 capital refers to equity and other forms of permanent capital that stays with the bank, as deposits and loans flow in and out. |

How are these bonds different from other debt instruments?

What did Yes Bank do?

What led to the write-off?

Implications

Must-Read Articles:

https://www.iasgyan.in/blogs/key-economic-concepts-back-to-basics

https://www.iasgyan.in/daily-current-affairs/prompt-corrective-action-framework

© 2026 iasgyan. All right reserved