Description

Context

- Over 50 per cent of agricultural households in the country were in debt with average outstanding loan per household at Rs 74,121 in 2019, says a survey conducted by National Statistical Office (NSO).

Details

- The survey further points out that only 69.6 per cent of the outstanding loans were taken from institutional sources like banks, cooperative societies and government agencies, while 20.5 per cent of loans were from professional moneylenders.

- Of the total loan, 57.5 per cent was taken for agricultural purposes.

- The findings of the survey — Situation Assessment of Agricultural Households and Land Holdings of Households in Rural India, 2019 — released by the Ministry of Programme Implementation and Statistics also estimated that the average monthly income from different sources rose to Rs 10,218 based on the ‘paid out expenses’ approach in 2018-19 compared with Rs 6,426 in 2012-13.

- The average outstanding loan per agricultural household increased 57.7 per cent to Rs 74,121 in 2018 compared with Rs 47,000 five years ago in 2013.

- While the national average outstanding loan was Rs 74,121 during July-December 2018, it was the highest in Andhra Pradesh at Rs 2.45 lakh and lowest in Nagaland at Rs 1,750.

Note:

- The survey defines an agricultural household as one receiving more than Rs 4,000 as value of produce from agri activities (e.g., cultivation of field crops, horticultural crops, fodder crops, plantation, animal husbandry, poultry, fishery, piggery, bee-keeping, vermiculture, sericulture, etc.) and having at least one member self-employed in agriculture either in principal status or in subsidiary status during the last 365 days.

Why farmers are in distress?

Past Indebtedness

- The root cause is past indebtedness. Rural debt is not only universal but hereditary.

- Ancestral debt is honoured in India and every villager considers it to be his sacred duty to repay the debt of his father.

Poverty

- Another cause of rural indebtedness is widespread poverty. With low income, fanners cannot save much.

- Thus, in case of an eventuality such as crop failure due to natural calamities like floods, or failure of monsoons, the farmer has to borrow—and often at a very high rate of interest.

Insurance fails to serve

- The Pradhan Mantri Fasal Bima Yojana was launched to provide insurance and financial support to farmers in the event of failure of any crops due to natural calamities, pests and diseases.

- It was also meant to stabilise the income of farmers and ensure they remain in farming.

- But the scheme has seen lower enrolments due to a string of factors, including high premiums and lack of innovation by insurance firms.

Collapsing farm prices

- Prices have collapsed for farm commodities.

- Low international prices have meant exports have been hit while imports have hurt prices at home.

- According to a Niti Aayog paper, on average, farmers do not realise remunerative prices due to limited reach of the minimum support prices (MSP) and an agricultural marketing system that delivers only a small fraction of the final price to the actual farmer.

Land Improvement

- Since land is the most important income-earning asset the farmers have a strong desire to make necessary improvements on land. With little or no saving farmers have to borrow to finance the cost of such improvements. Consequently, they fall into a ‘debt trap’.

Social and Other Obligations

- Farmers also fall in debt because they have to discharge certain social obligations irrespective of their means and resources. They have to observe religious and social functions.

- They also borrow to meet consumption needs.

Moneylenders

- They not only charge excessive interest but maintain false accounts.

- When the amount of debt gets accumulated over a number of years the farmer finds it difficult to repay it and is forced to surrender his land to the moneylender.

- This is the plight of the rural masses in India even today.

Bottlenecks in Institutional finance

- Institutional finance is subject to complicated formalities and rigid repayment conditions.

- The moneylender’s methods are such as to confiscate all the resources of the debtor.

- The cooperative societies do a lot of favouritism and give loans mostly for short-term production purposes. Medium and long-term institutional finance is grossly inadequate compared to needs.

Irrigation takes a hit

- Irrigation is crucial for the farm sector, where large tracts of land still depend on monsoon rains.

- Experts say a number of factors, including bureaucratic delays and slow implementation by states, have hurt progress for this crucial input.

Marketing is ignored

- According to a NITI Aayog, farm sector development has ignored the potential of marketing.

- Archaic laws still hobble the sector.

- Access of farmers to well-developed markets remains an issue although several initiatives have been launched to develop an electronic market place.

- Reforms to the APMC Act have been slow and most states have dragged their feet on it.

- Experts suggest an entity such as the GST Council to bring together states and the Centre to jointly take decisions to reform the sector and provide better access to markets for farmers.

- According to the Organisation for Economic Cooperation and Development (OECD), the combination of market regulations and infrastructure deficiencies leads to a price depressing effect on the sector.

Modern tech missing

- Introduction of latest technology has been limited due to a number of reasons.

- Access to modern technology could act as a boost to productivity through improved variety of seeds, farm implements and farming technology.

- According to a Niti Aayog, there has been no real technological breakthrough in recent times.

Fragmented supply chains

- Large gaps in storage, cold chains and limited connectivity have added to the woes of farmers.

- It has also added to the significant post-harvest losses of fruit and vegetables, estimated at 4% to 16% of the total output, according to the OECD.

Lack of food processing clusters

- This has meant that there is little incentives for farmers to diversify.

- According to an OECD, share of high-value sectors in food processing is low with fruit, vegetable and meat products accounting for 5% and 8% of the total value of output compared to cereal based products at 21% and oilseeds at 18%.

Delayed FCI reforms

- Shanta Kumar Committee had recommended that FCI hand over all procurement operations of wheat, paddy and rice to states that have gained sufficient experience in this regard and have created reasonable infrastructure for procurement.

- These states are Andhra Pradesh, Chhattisgarh, Haryana, Madhya Pradesh.

- It had suggested a complete overhaul of FCI and recommended that farmers be given direct cash subsidy (of about Rs 7000/ha) and fertiliser sector deregulated.

- The panel had said direct cash subsidy to farmers will go a long way to help those who take loans from money lenders at exorbitant interest rates to buy fertilisers or other inputs, thus relieving some distress in the agrarian sector.

- FCI should outsource its stocking operations to various agencies such as Central Warehousing Corporation (CWC), State Warehousing Corporation (SWC), Private Sector under Private Entrepreneur Guarantee (PEG) scheme.

- The report has been put in cold storage.

Low productivity

- According to OECD data, 85% of operational land holdings are less than 2 hectares and account for 45% of the total cropped area.

- Only 5% of farmers work on land holding larger than 4 hectares, according to the Agricultural Census, 2016. Productivity lags other Asian economies such as China, Vietnam and Thailand and average yields are low compared to other global producers.

- Wheat and rice yields are nearly 3 times lower than world yields while those for mango, banana, onion or potato are between 2 and 7 times lower than the highest yields achieved globally, according to the OECD.

Farmers' Suicide

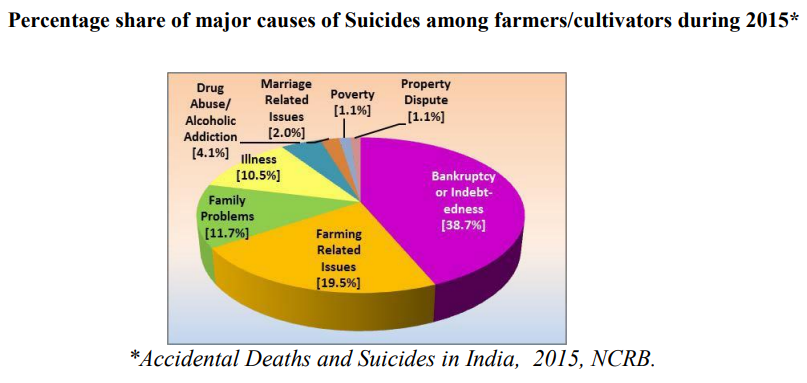

- Indebtedness and farmers' suicide is closely linked. The vicious cycle of debt has aggravated the agrarian crisis leading to increase in the number of farmers suicide.

- According to the "National Crime Records Bureau's (NCRB) Report "Accidental Deaths and Suicides in India 2015", a total of 8007 cultivators/farmers had committed suicide in 2015.

Initiatives taken to reduce debt burden of farmers

- For development of agriculture and welfare of farmers of the country, the Government in DAC&FW, is implementing various Central Sector/ Centrally Sponsored Schemes, which include:

- RashtriyaKrishiVikasYojana (RKVY)

- National Food Security Mission (NFSM)

- National Agriculture Market (e-NAM)

- National Mission For Sustainable Agriculture (NMSA)

- Pradhan MantriFasalBimaYojana (PMFBY) provides a comprehensive insurance cover against failure of insured crops due to non-preventable natural risks, thus providing financial support to farmers suffering crop loss/ damage arising out of unforeseen events; stabilizing the income of farmers to ensure their continuance in farming; and encouraging them to adopt innovative and modern agricultural practices.

- Pradhan MantriKIsanSAmmanNidhi (PM-KISAN) Scheme has been implemented to provide an assured income support to all farmers, irrespective of the size of their land holdings subject to the exclusion factor. Under this scheme direct income support @ of Rs. 6,000 per year will be transferred directly into the bank accounts of beneficiary farmers, in three equal instalments of Rs.2,000 each.

- To bring small, marginal, tenant farmers, oral lessees, etc. into the fold of institutional credit, Joint Liability Groups (JLGs) have been promoted by banks.

- With a view to ensure availability of agriculture credit at a reduced interest rate of 7% p.a. to the farmers, the Government of India in the Department of Agriculture Cooperation and Farmers’ Welfare (DAC&FW) implements an Interest Subvention Scheme for short term crop loans up to Rs. 3.00 lakh.

- The Scheme provides interest subvention of 2% per annum to Banks on use of their own resources. Besides, additional 3% incentive is given to the farmers for prompt repayment of the loan, thereby reducing the effective rate of interest to 4%.

- To enhance coverage of small and marginal farmers in the formal credit system, RBI has decided to raise the limit for collateral-free agriculture loans from Rs. 1 lakh to Rs. 1.6 lakh.

- The requirement of ‘no due’ certificate has also been dispensed with for small loans upto Rs.50,000/- to small and marginal farmers, share croppers and the like and, instead, only a self-declaration from the borrower is required.

- The Union Cabinet in 2020 approved a new pan India Central Sector Scheme called Agriculture Infrastructure Fund.

- The scheme shall provide a medium - long term debt financing facility for investment in viable projects for post-harvest management Infrastructure and community farming assets through interest subvention and financial support.

- The benefit of interest subvention scheme has been extended to small and marginal farmers having Kisan Credit Card for a further period upto six months post harvest on the same rate as available to crop loan against negotiable warehouse receipt.

- Farm Loan Waiver: The waivers are primarily meant to discourage suicides by farmers due to widespread indebtedness.

- The new Farm Bills: Read here, https://www.iasgyan.in/blogs/farm-laws-2020-and-farmers-protest-explained

Conclusion

- Indebtedness in one form or another has been in existence for centuries.

- Measures like loan waiver can provide only a temporary relief, but long term solutions are needed to solve farmers woes.

- There is a pressing need for implementing Shanta Kumar Committee recommendations.

Read about the recommendations in detail here: https://pib.gov.in/newsite/PrintRelease.aspx?relid=114860

- A transparent liquidation policy is the need of hour, which should automatically kick in when FCI is faced with surplus stocks than buffer norms.

- Greater flexibility to FCI with business orientation to operate in OMSS and export markets is needed.

https://www.pib.gov.in/PressReleasePage.aspx?PRID=1753856

https://indianexpress.com/article/india/average-debt-of-farm-households-up-57-in-five-years-till-2018-7501765/